A CBDC, or central bank digital currency, is a digital form of a country’s official fiat money, issued and backed directly by its central bank. It’s the same unit of account as the cash in your wallet (a digital dollar, euro or yuan) but it lives as an electronic claim on the central bank rather than a banknote or a balance at a commercial bank.

Putting the central bank directly behind the digital money the public spends is the design choice that makes CBDCs both powerful and deeply controversial.

The numbers capture the moment. As of 2026, the Atlantic Council’s CBDC Tracker counts 137 countries and currency unions (roughly 98% of global GDP) exploring a CBDC, up from just 35 in 2020. Only three have fully launched a retail version. That chasm between exploring and adopting is the real story of CBDCs today.

Key Takeaways

- A CBDC is a digital version of fiat currency issued by a central bank.

- CBDCs are centralized, unlike Bitcoin and most cryptocurrencies.

- They can be designed for retail payments, wholesale settlement between banks, or cross-border transfers.

- Supporters argue CBDCs can modernize payments, cut costs and widen financial inclusion.

- Critics warn they could enable surveillance, censorship and tighter control over how money is spent.

- The deepest difference between a CBDC and Bitcoin is control: a CBDC is state-issued and permissioned, while Bitcoin is decentralized and can be self-custodied.

What Is a CBDC?

CBDC stands for central bank digital currency: a digital form of a nation’s fiat currency that is a direct liability of the central bank. The central bank itself stands behind it, exactly as it stands behind physical cash.

That backing is what separates a CBDC from the digital money most people already use. The balance in your banking app is a commercial bank deposit, a claim on a private bank, not on the central bank. A CBDC strips out that intermediary, making the money itself central bank money in digital form. It also differs from decentralized cryptocurrencies like Bitcoin, which have no issuer at all, and from stablecoins, which are issued by private companies.

Depending on its design, a CBDC can serve as everyday payment, a settlement asset between financial institutions, or a tool for distributing government funds and steering monetary policy. There is no single CBDC model, as the term spans a wide range of designs that differ sharply in how much privacy, programmability and control they bake in.

How Does a CBDC Work?

At its simplest: a central bank issues the digital currency, users hold and spend it through wallets or accounts, and every transaction is recorded on a ledger the central bank or its partners maintain. The practical sequence:

- A central bank creates or authorizes the digital currency as legal central bank money.

- Users access it through wallets, apps, banks or licensed payment providers.

- Transactions are recorded on a ledger or database.

- Some designs use blockchain or distributed ledger technology; many use conventional centralized infrastructure.

- The central bank keeps ultimate control over issuance and the monetary rules.

- Some designs support offline payments; some allow programmable conditions.

One stubborn misconception is that CBDCs must run on a blockchain. Many don’t. China’s e-CNY, the largest CBDC project in the world, runs primarily on centralized infrastructure rather than a public blockchain. Whether a CBDC uses distributed ledger technology is a design choice rather than a defining trait, and it matters, because the architecture shapes how traceable and controllable the money becomes.

CBDC vs. Cash, Bank Deposits, Stablecoins and Bitcoin

The fastest way to grasp a CBDC is to set it beside the other forms of money it sits between.

FeatureCashBank depositCBDCStablecoinBitcoinIssuerCentral bankCommercial bankCentral bankPrivate company or protocolNo central issuerFormPhysicalDigital account balanceDigital fiat currencyDigital tokenDigital assetLiability ofCentral bankCommercial bankCentral bankIssuer / reservesNo issuer liabilityCentralized?Yes, but peer-to-peer in useYesYesUsually yesNoNeeds internet?NoUsuallyUsually, except offline designsYesYesPrivacyHigh in personLow to mediumDepends on design, often below cashLow to mediumPseudonymous, not anonymousCan be frozen?Hard to freezeYesPotentiallyUsuallyNot at the protocol levelSupplyCentral bank controlledBank credit creationCentral bank controlledDepends on issuerFixed schedule, 21M capMain useEveryday paymentsSavings and paymentsDigital fiat paymentsCrypto payments and tradingStore of value, P2P moneyFeatureIssuerCashCentral bankBank depositCommercial bankCBDCCentral bankStablecoinPrivate company or protocolBitcoinNo central issuerFeatureFormCashPhysicalBank depositDigital account balanceCBDCDigital fiat currencyStablecoinDigital tokenBitcoinDigital assetFeatureLiability ofCashCentral bankBank depositCommercial bankCBDCCentral bankStablecoinIssuer / reservesBitcoinNo issuer liabilityFeatureCentralized?CashYes, but peer-to-peer in useBank depositYesCBDCYesStablecoinUsually yesBitcoinNoFeatureNeeds internet?CashNoBank depositUsuallyCBDCUsually, except offline designsStablecoinYesBitcoinYesFeaturePrivacyCashHigh in personBank depositLow to mediumCBDCDepends on design, often below cashStablecoinLow to mediumBitcoinPseudonymous, not anonymousFeatureCan be frozen?CashHard to freezeBank depositYesCBDCPotentiallyStablecoinUsuallyBitcoinNot at the protocol levelFeatureSupplyCashCentral bank controlledBank depositBank credit creationCBDCCentral bank controlledStablecoinDepends on issuerBitcoinFixed schedule, 21M capFeatureMain useCashEveryday paymentsBank depositSavings and paymentsCBDCDigital fiat paymentsStablecoinCrypto payments and tradingBitcoinStore of value, P2P money

Two rows carry the weight of the whole debate. Privacy is where CBDCs draw the most fire: cash is private by default, while a CBDC’s privacy depends entirely on how it’s built. And the “can be frozen?” row captures the philosophical divide.

A commercial deposit or a CBDC can in principle be blocked by its issuer, whereas Bitcoin held in self-custody cannot be frozen at the network level. That single property makes CBDCs attractive to policymakers and alarming to civil-liberties advocates, for exactly the same reason.

Types of CBDCs

CBDCs are usually grouped by who uses them and how they are accessed.

CBDC typeWhat it meansWho uses itExample use caseRetail CBDCDigital central bank money for the publicIndividuals and businessesEveryday paymentsWholesale CBDCDigital central bank money for institutionsBanks and financial firmsInterbank settlementDirect CBDCCentral bank manages user accounts directlyPublic or institutionsCentral-bank-run payment systemIndirect CBDCPrivate intermediaries handle customer servicesPublic via banks/fintechsBank-distributed CBDCHybrid CBDCCentral bank issues; intermediaries serve usersPublic via institutionsTwo-tier CBDC systemAccount-based CBDCAccess tied to a verified identityUsers with KYC accountsIdentity-linked paymentsToken-based CBDCAccess via possession of a digital tokenUsers with wallets/devicesCash-like digital paymentOffline CBDCWorks without continuous internetPublicDisaster and remote-area paymentsProgrammable CBDCCarries built-in rules or conditionsGovernments, institutions, usersTargeted or restricted spendingCBDC typeRetail CBDCWhat it meansDigital central bank money for the publicWho uses itIndividuals and businessesExample use caseEveryday paymentsCBDC typeWholesale CBDCWhat it meansDigital central bank money for institutionsWho uses itBanks and financial firmsExample use caseInterbank settlementCBDC typeDirect CBDCWhat it meansCentral bank manages user accounts directlyWho uses itPublic or institutionsExample use caseCentral-bank-run payment systemCBDC typeIndirect CBDCWhat it meansPrivate intermediaries handle customer servicesWho uses itPublic via banks/fintechsExample use caseBank-distributed CBDCCBDC typeHybrid CBDCWhat it meansCentral bank issues; intermediaries serve usersWho uses itPublic via institutionsExample use caseTwo-tier CBDC systemCBDC typeAccount-based CBDCWhat it meansAccess tied to a verified identityWho uses itUsers with KYC accountsExample use caseIdentity-linked paymentsCBDC typeToken-based CBDCWhat it meansAccess via possession of a digital tokenWho uses itUsers with wallets/devicesExample use caseCash-like digital paymentCBDC typeOffline CBDCWhat it meansWorks without continuous internetWho uses itPublicExample use caseDisaster and remote-area paymentsCBDC typeProgrammable CBDCWhat it meansCarries built-in rules or conditionsWho uses itGovernments, institutions, usersExample use caseTargeted or restricted spending

Two distinctions matter most: retail vs. wholesale, and account-based vs. token-based. Most live and piloted CBDCs use a hybrid, two-tier model. The central bank issues the currency while commercial banks and payment firms handle wallets and customer service. Wholesale CBDCs, used only between financial institutions, are advancing faster and with far less controversy than retail versions, because they never touch ordinary people’s day-to-day spending.

Why Are Central Banks Exploring CBDCs?

Central banks give a consistent set of reasons for the global rush into CBDC research:

- Modernizing aging payment infrastructure

- Reducing settlement times and cash-handling costs

- Improving slow, expensive cross-border payments

- Supporting financial inclusion for the unbanked

- Competing with private stablecoins and big-tech payment systems

- Preserving a role for public money as economies go digital

- Distributing government payments more directly

- Strengthening anti-money-laundering (AML) and know-your-customer (KYC) monitoring

- Experimenting with new monetary policy tools

The competitive motive is increasingly explicit. The ECB frames the digital euro partly as a matter of European “strategic autonomy,” less reliance on foreign card networks and private stablecoins. China ties its e-CNY to the longer game of internationalizing the yuan. A CBDC, in other words, is as much a geopolitical project as a payments one.

The monetary-policy motive is easy to underrate until you see how blunt the existing toolkit can be. The Fed’s primary lever, the federal funds rate, has spent long stretches pinned near zero, through much of 2009–2015 and again in 2020–2022 (Figure 1), leaving little room to ease further in a downturn. A retail CBDC, some economists argue, would open a more direct channel to households and, far more controversially, a way to push rates below zero on digital balances once the conventional tool is exhausted.

Figure 1. U.S. federal funds effective rate, 1955–2025 | Source: FRED

Figure 1. U.S. federal funds effective rate, 1955–2025 | Source: FRED

Potential Benefits of CBDCs

A fair assessment has to take the upside seriously, and pair each claim with its real-world caveat.

Potential benefitExplanationImportant caveatFaster paymentsNear-instant settlementMany countries already have fast payment railsLower costsCheaper digital settlementHigh build and compliance costsFinancial inclusionDigital payments for the unbankedNeeds phones, IDs, internet and trustCross-border paymentsSimpler international settlementRequires coordination between countriesReduced counterfeitingHard to physically counterfeitCybersecurity risk remainsDirect government paymentsFaster stimulus and benefitsRaises control and surveillance questionsProgrammabilityRules can be attached to moneyCan erode financial freedomMonetary policy toolsMore direct policy transmissionCan deepen central bank power over individualsPotential benefitFaster paymentsExplanationNear-instant settlementImportant caveatMany countries already have fast payment railsPotential benefitLower costsExplanationCheaper digital settlementImportant caveatHigh build and compliance costsPotential benefitFinancial inclusionExplanationDigital payments for the unbankedImportant caveatNeeds phones, IDs, internet and trustPotential benefitCross-border paymentsExplanationSimpler international settlementImportant caveatRequires coordination between countriesPotential benefitReduced counterfeitingExplanationHard to physically counterfeitImportant caveatCybersecurity risk remainsPotential benefitDirect government paymentsExplanationFaster stimulus and benefitsImportant caveatRaises control and surveillance questionsPotential benefitProgrammabilityExplanationRules can be attached to moneyImportant caveatCan erode financial freedomPotential benefitMonetary policy toolsExplanationMore direct policy transmissionImportant caveatCan deepen central bank power over individuals

The honest read: several headline benefits are weaker than they sound in countries that already run modern, instant payment systems. The strongest case for a retail CBDC tends to be in economies with large unbanked populations and weak payment rails, which is precisely where the three live retail CBDCs launched.

Risks and Criticisms of CBDCs

The criticisms cluster around control, privacy and financial stability.

RiskWhy it mattersThe self-custody anglePrivacy lossCBDCs may be more traceable than cashPrivacy tools and self-custody gain importanceSurveillanceCentralized ledgers enable broad monitoringBitcoin offers a permissionless alternativeCensorshipPayments could be blocked or restrictedBitcoin is censorship-resistant at the network levelProgrammable limitsSpending rules, expiry dates or capsUsers may lose control over their own moneyCybersecurityA national system is a prime attack targetDecentralization removes single points of failureBank disintermediationDeposits may flow out of banksCould disrupt lending and stabilityFaster bank runsDeposit flight could accelerate in a crisisHolding limits may be requiredCentralized powerMore direct state control over moneyBitcoin separates money from authorityNegative interest ratesEasier to impose on digital balancesRaises concerns over savings and autonomyAdoption failureUsers may not want or trust themEarly real-world uptake has been weakRiskPrivacy lossWhy it mattersCBDCs may be more traceable than cashThe self-custody anglePrivacy tools and self-custody gain importanceRiskSurveillanceWhy it mattersCentralized ledgers enable broad monitoringThe self-custody angleBitcoin offers a permissionless alternativeRiskCensorshipWhy it mattersPayments could be blocked or restrictedThe self-custody angleBitcoin is censorship-resistant at the network levelRiskProgrammable limitsWhy it mattersSpending rules, expiry dates or capsThe self-custody angleUsers may lose control over their own moneyRiskCybersecurityWhy it mattersA national system is a prime attack targetThe self-custody angleDecentralization removes single points of failureRiskBank disintermediationWhy it mattersDeposits may flow out of banksThe self-custody angleCould disrupt lending and stabilityRiskFaster bank runsWhy it mattersDeposit flight could accelerate in a crisisThe self-custody angleHolding limits may be requiredRiskCentralized powerWhy it mattersMore direct state control over moneyThe self-custody angleBitcoin separates money from authorityRiskNegative interest ratesWhy it mattersEasier to impose on digital balancesThe self-custody angleRaises concerns over savings and autonomyRiskAdoption failureWhy it mattersUsers may not want or trust themThe self-custody angleEarly real-world uptake has been weak

The recurring theme: a CBDC’s most useful features for a government (traceability, programmability, direct reach) are the same ones that worry privacy and human-rights advocates. The danger lives less in digital money itself than in the design choices about how much privacy and user control to preserve.

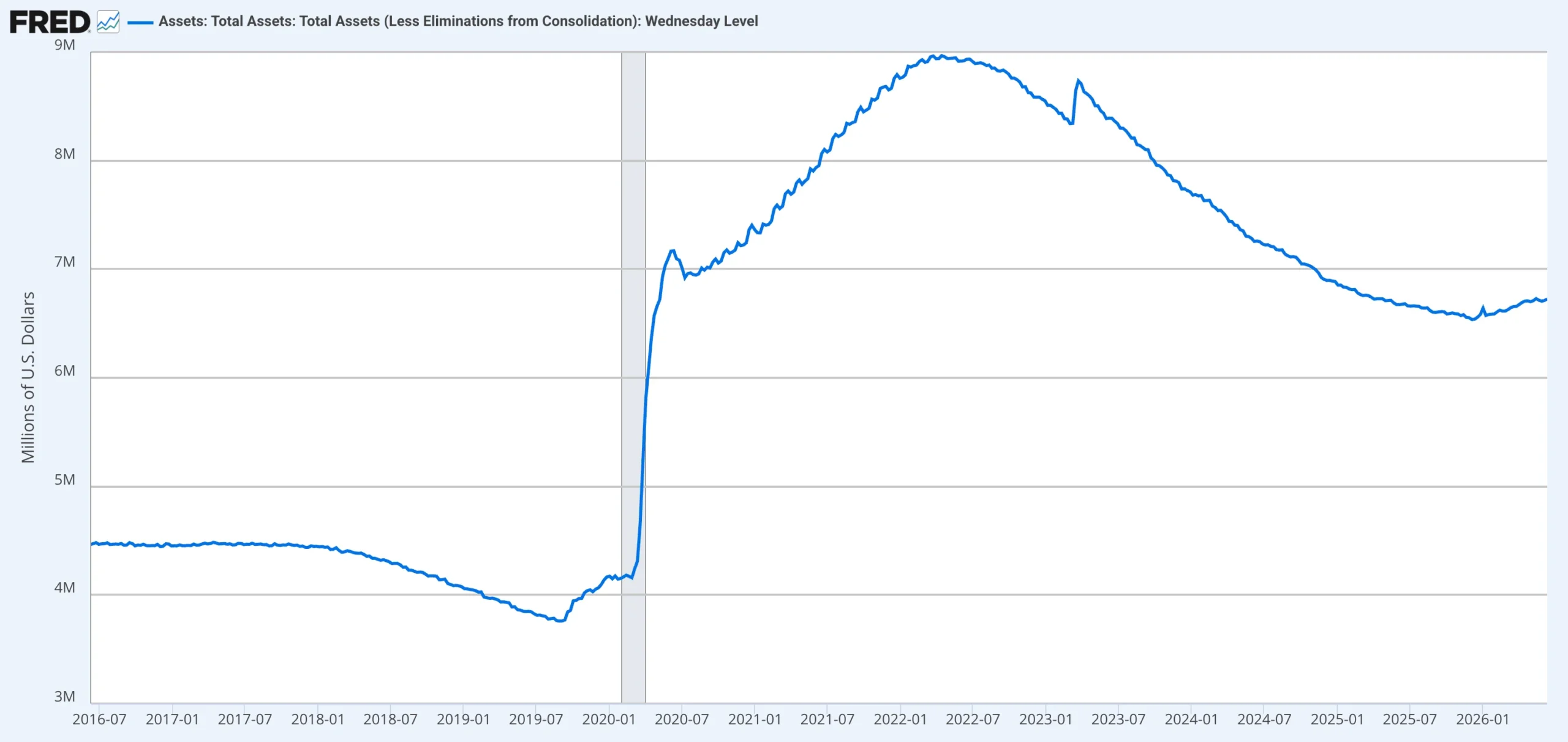

That worry about concentrated power doesn’t come from nowhere. Central banks already wield sweeping discretion over the money supply. The Federal Reserve’s balance sheet roughly doubled, from about $4 trillion to nearly $9 trillion, in barely two years after 2020 (Figure 2).

The fear is not that such tools exist, but that a retail CBDC would extend that reach all the way down to individual wallets, pairing balance-sheet-scale power with transaction-level visibility and control.

Figure 2. Total assets of the Federal Reserve, 2016–2026. | Source: FRED

Figure 2. Total assets of the Federal Reserve, 2016–2026. | Source: FRED

CBDC Privacy and Surveillance Concerns

Privacy is the single most contested issue in the CBDC debate, and no one framed the stakes more candidly than the head of the central banks’ central bank. At a 2020 IMF seminar, Bank for International Settlements General Manager Agustín Carstens spelled out the difference between a banknote and a CBDC:

We don’t know who’s using a $100 bill today and we don’t know who’s using a 1,000 peso bill today. The key difference with the CBDC is the central bank will have absolute control on the rules and regulations that will determine the use of that expression of central bank liability, and also we will have the technology to enforce that. | Agustín Carstens, General Manager of the Bank for International Settlements

Critics treat that as a warning; Carstens offered it as a design fact. Both readings are correct, which is the whole problem. Where the lines actually fall:

- A CBDC can be less private than physical cash, depending on its design.

- Transactions may be logged in centralized systems the state can access.

- Wallets often require identity verification, and KYC/AML rules typically apply.

- Law enforcement may be able to reach transaction data.

- Some designs propose privacy thresholds for small payments.

- “Privacy-preserving” is not the same as “anonymous.”

Central banks building retail CBDCs insist strong privacy is achievable. The ECB says the digital euro would meet the highest privacy standards and that, by design, the central bank would “not have access to personal data,” with offline payments offering cash-like privacy. Even inside the U.S. Federal Reserve, Governor Michelle Bowman has warned that a poorly designed CBDC could politicize the payments system.

The civil-liberties critique runs deeper than data collection. The Human Rights Foundation, which maintains its own CBDC tracker, notes that unlike cash, CBDCs “can even have expiration dates or blacklists.” That is where the Bitcoin contrast turns concrete: an open, self-custodiable money cannot be programmed to expire, blacklist a user, or report on its holder, even though Bitcoin itself is only pseudonymous, not fully private.

Programmable Money and What CBDCs Could Enable

Programmability is the feature that most separates a CBDC from a mere digital copy of cash. Money with rules attached can do things banknotes never could, for better and worse.

Programmable featurePotential benefitPotential riskExpiring paymentsEncourages spending during stimulusReduces user autonomyCategory restrictionsEnsures funds are used as intendedCreates permissioned moneyGeofencingSupports local or disaster aidLimits where people can spendTransaction limitsManages fraud and riskRestricts financial freedomAutomatic complianceReduces illicit financeIncreases surveillanceNegative ratesA new policy leverPenalizes savingDirect stimulusSpeeds government transfersExpands control over spendingProgrammable featureExpiring paymentsPotential benefitEncourages spending during stimulusPotential riskReduces user autonomyProgrammable featureCategory restrictionsPotential benefitEnsures funds are used as intendedPotential riskCreates permissioned moneyProgrammable featureGeofencingPotential benefitSupports local or disaster aidPotential riskLimits where people can spendProgrammable featureTransaction limitsPotential benefitManages fraud and riskPotential riskRestricts financial freedomProgrammable featureAutomatic compliancePotential benefitReduces illicit financePotential riskIncreases surveillanceProgrammable featureNegative ratesPotential benefitA new policy leverPotential riskPenalizes savingProgrammable featureDirect stimulusPotential benefitSpeeds government transfersPotential riskExpands control over spending

Money that can be told where, when and on what it may be spent sounds like science fiction — and it is: the 2011 film In Time imagines a world where currency comes with a countdown clock and the poor literally run out of time. A programmable CBDC need not be that dystopian, but it makes the thought experiment real. The same mechanism that lets a government rush disaster relief to a flooded region can also dictate what citizens buy, where, and by when they must spend it. Whether programmability reads as convenience or control depends entirely on who writes the rules and what limits constrain them.

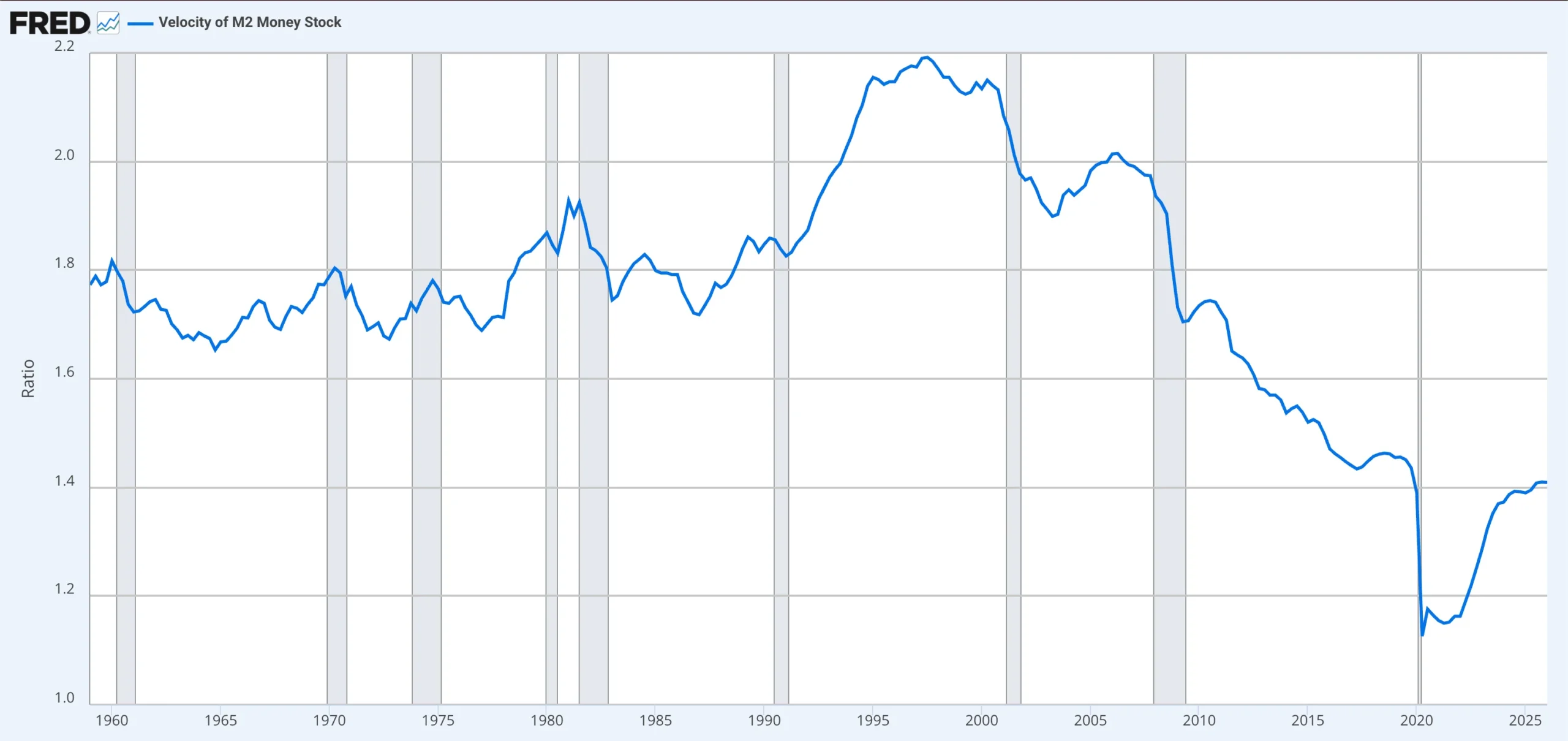

This is not purely abstract economics. The velocity of money — how often each dollar changes hands in a given period — has trended down for decades and collapsed in 2020 (Figure 3), a pattern that frustrates policymakers trying to stimulate demand. Expiring balances, geofenced relief and direct programmable transfers are, among other things, levers aimed at exactly that problem: money engineered to be spent rather than held. The same dial that can revive a stalled economy can also override an individual’s choice to save.

Figure 3. Velocity of M2 money stock, 1960–2025 | Source: FRED

Figure 3. Velocity of M2 money stock, 1960–2025 | Source: FRED

Which Countries Have CBDCs?

The global map ranges from three live retail launches to dozens of pilots and a few notable retreats. Status changes quickly, so treat this as a 2026 snapshot to verify before relying on it.

Country / regionCBDC nameStatus (2026)TypeNotesBahamasSand DollarLaunchedRetailOne of the first national CBDCsNigeriaeNairaLaunchedRetailAdoption has been slowJamaicaJam-DexLaunchedRetailCaribbean retail exampleChinaDigital yuan / e-CNYAdvanced pilotRetailWorld’s largest pilotEuropean UnionDigital euroPreparation phaseRetailIssuance decision pending EU lawUnited StatesDigital dollarBlocked / no CBDC—Federal CBDC barred by executive orderUnited KingdomDigital poundDesign phaseRetailBank of England “Digital Pound Lab”IndiaDigital rupee (e₹)PilotRetail and wholesaleLarge emerging-market pilotBrazilDrexPilotWholesale / tokenizedLatin America’s flagship projectRussiaDigital rublePhased rolloutRetailSanctions and geopolitics relevantAustralia—Research / pilotsWholesale focusInstitutional use casesCanada—ResearchRetail conceptNo launch plannedCountry / regionBahamasCBDC nameSand DollarStatus (2026)LaunchedTypeRetailNotesOne of the first national CBDCsCountry / regionNigeriaCBDC nameeNairaStatus (2026)LaunchedTypeRetailNotesAdoption has been slowCountry / regionJamaicaCBDC nameJam-DexStatus (2026)LaunchedTypeRetailNotesCaribbean retail exampleCountry / regionChinaCBDC nameDigital yuan / e-CNYStatus (2026)Advanced pilotTypeRetailNotesWorld’s largest pilotCountry / regionEuropean UnionCBDC nameDigital euroStatus (2026)Preparation phaseTypeRetailNotesIssuance decision pending EU lawCountry / regionUnited StatesCBDC nameDigital dollarStatus (2026)Blocked / no CBDCType—NotesFederal CBDC barred by executive orderCountry / regionUnited KingdomCBDC nameDigital poundStatus (2026)Design phaseTypeRetailNotesBank of England “Digital Pound Lab”Country / regionIndiaCBDC nameDigital rupee (e₹)Status (2026)PilotTypeRetail and wholesaleNotesLarge emerging-market pilotCountry / regionBrazilCBDC nameDrexStatus (2026)PilotTypeWholesale / tokenizedNotesLatin America’s flagship projectCountry / regionRussiaCBDC nameDigital rubleStatus (2026)Phased rolloutTypeRetailNotesSanctions and geopolitics relevantCountry / regionAustraliaCBDC name—Status (2026)Research / pilotsTypeWholesale focusNotesInstitutional use casesCountry / regionCanadaCBDC name—Status (2026)ResearchTypeRetail conceptNotesNo launch planned

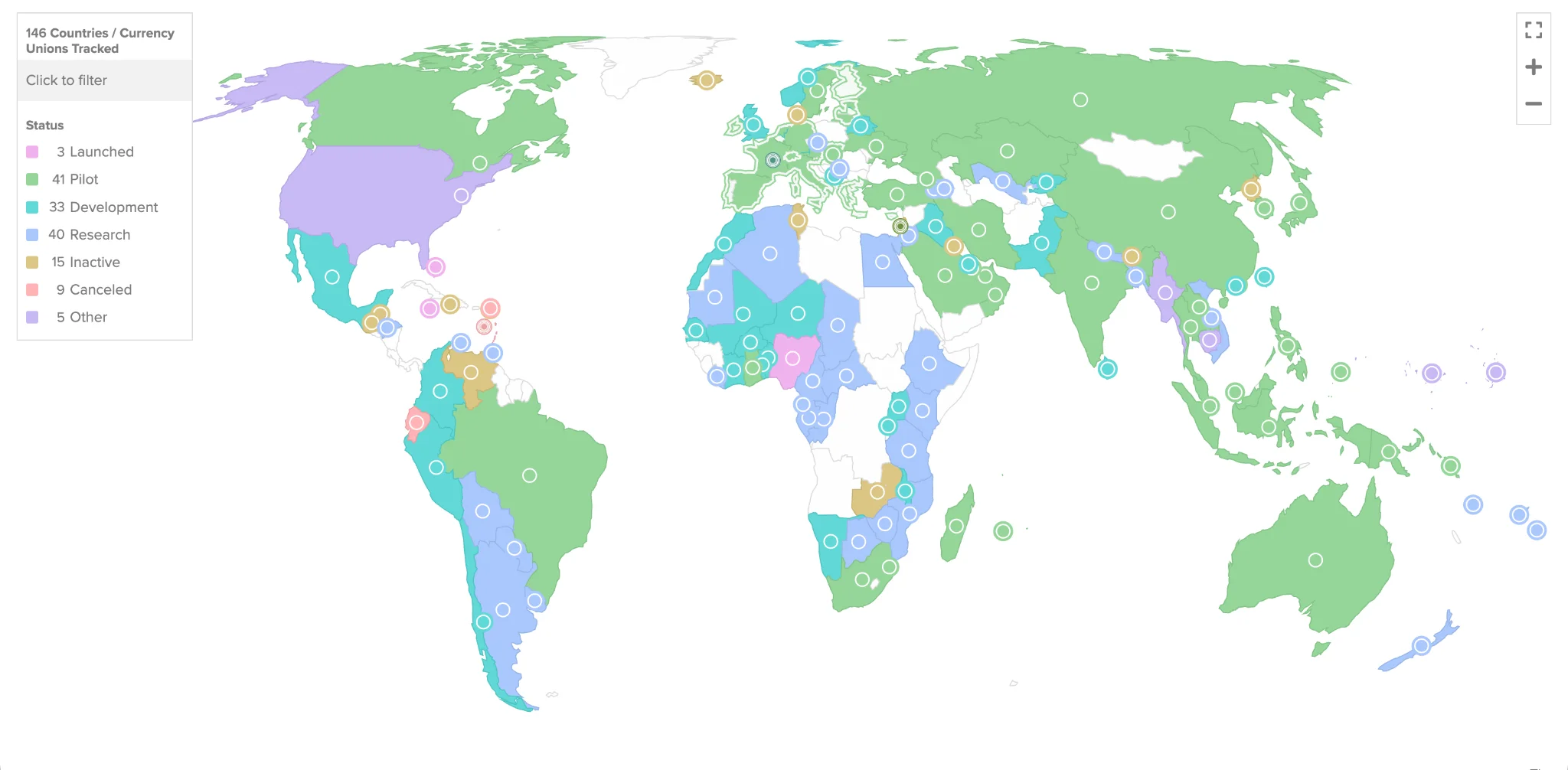

A single map captures the unevenness better than any table. Plotting each country by stage (live retail launch, advanced pilot, design or research phase, and outright ban) shows just how lopsided the field is: a vast crowd of explorers, a thin scattering of adopters, and a few notable refusers (Figure 4).

Global CBDC development stages (2026)

Global CBDC development stages (2026)

China’s e-CNY dwarfs every rival: cumulative transactions topped roughly 16.7 trillion yuan (about US$2.3 trillion) by late 2025, spread across pilots in dozens of cities and wired into Alipay and WeChat Pay. Yet even there, everyday retail use has trailed official ambition, and Nigeria’s eNaira fared worse, with adoption stuck in the low single digits despite a hard government push. The pattern across the live examples is unmistakable, and a little deflating for central planners: building a CBDC turns out to be far easier than persuading anyone to use one.

Does the US Have a CBDC?

No. The United States has no retail CBDC, and it has moved decisively against one. The Federal Reserve’s official posture was always caution rather than rejection. Chair Jerome Powell summed it up:

We do not need to be first. We need to get it right. And getting it right means that we not only look at the potential benefits of a CBDC, but also the potential risks. | Jerome Powell, Chair of the U.S. Federal Reserve

Politics then carried “getting it right” all the way to “not at all.” The “digital dollar” remains a concept, never a product, and the policy direction has reversed through three moves in 2025.

Legislation / actionDateWhat it didExecutive Order 14178Jan 2025Banned federal agencies from establishing or promoting a U.S. CBDC.Anti-CBDC Surveillance State ActJuly 2025Passed the House; explicitly bars the Fed from issuing a retail CBDC directly or via banks.The GENIUS ActJuly 2025Signed into law; established a framework to encourage private dollar stablecoins over a public CBDC.Legislation / actionExecutive Order 14178DateJan 2025What it didBanned federal agencies from establishing or promoting a U.S. CBDC.Legislation / actionAnti-CBDC Surveillance State ActDateJuly 2025What it didPassed the House; explicitly bars the Fed from issuing a retail CBDC directly or via banks.Legislation / actionThe GENIUS ActDateJuly 2025What it didSigned into law; established a framework to encourage private dollar stablecoins over a public CBDC.

As of 2026, the Anti-CBDC Surveillance State Act has cleared the House but not the Senate. The GENIUS Act is a separate law governing private dollar stablecoins, and together the three reflect a deliberate strategy: encourage privately issued digital dollars while rejecting a government-issued one.

The bet behind that strategy is that the private market can already do the job. Tether (USDT), the largest dollar-pegged stablecoin, has swelled from a few billion dollars in 2020 to well over $180 billion (Figure 5). To U.S. lawmakers, that trajectory is evidence a public CBDC is simply unnecessary; to skeptics, it relocates the same questions about issuer power and reserve backing into private hands.

Figure 5. Market capitalization of USDT (Tether), 2020–2026 | Source: TradingView

Figure 5. Market capitalization of USDT (Tether), 2020–2026 | Source: TradingView

A few terms get tangled in this debate, so it helps to keep them straight.

TermMeaningDigital dollarGeneral term for a possible US CBDCUS CBDCA potential Fed-issued central bank digital currencyFedNowA real-time interbank payment system — not a CBDCStablecoinA privately issued token pegged to fiat, e.g. USDC or USDTTokenized depositA commercial bank deposit represented digitally, not central bank moneyTermDigital dollarMeaningGeneral term for a possible US CBDCTermUS CBDCMeaningA potential Fed-issued central bank digital currencyTermFedNowMeaningA real-time interbank payment system — not a CBDCTermStablecoinMeaningA privately issued token pegged to fiat, e.g. USDC or USDTTermTokenized depositMeaningA commercial bank deposit represented digitally, not central bank money

The most common error is treating FedNow as a stealth CBDC. It is not. FedNow is a settlement service connecting banks; it creates no new form of central bank money for the public. The American stance contrasts sharply with the EU and China, and privacy and financial-freedom concerns sat at the center of the political case against a U.S. CBDC.

CBDCs vs. Bitcoin

This is the comparison that matters most, because CBDCs and Bitcoin are opposite answers to the same question: who should control digital money?

FeatureCBDCBitcoinIssuerCentral bankNo issuerGovernanceGovernment / central bankDecentralized network consensusSupplySet by monetary authorityFixed cap of 21 million BTCAccessMay require identity verificationPermissionlessCustodyVia approved wallets/providersCan be self-custodiedCensorship resistanceDepends on design; potentially censorableStrong at the protocol levelPrivacyDesign-dependent; may be highly traceablePublic but pseudonymousMonetary policyCentral bank controlledFixed by protocolSettlementCentralized or permissionedDecentralized blockchainMain purposeDigital fiat moneyDecentralized, scarce digital moneyFeatureIssuerCBDCCentral bankBitcoinNo issuerFeatureGovernanceCBDCGovernment / central bankBitcoinDecentralized network consensusFeatureSupplyCBDCSet by monetary authorityBitcoinFixed cap of 21 million BTCFeatureAccessCBDCMay require identity verificationBitcoinPermissionlessFeatureCustodyCBDCVia approved wallets/providersBitcoinCan be self-custodiedFeatureCensorship resistanceCBDCDepends on design; potentially censorableBitcoinStrong at the protocol levelFeaturePrivacyCBDCDesign-dependent; may be highly traceableBitcoinPublic but pseudonymousFeatureMonetary policyCBDCCentral bank controlledBitcoinFixed by protocolFeatureSettlementCBDCCentralized or permissionedBitcoinDecentralized blockchainFeatureMain purposeCBDCDigital fiat moneyBitcoinDecentralized, scarce digital money

No one has put the critics’ case more bluntly than Edward Snowden, who used his own platform to savage the concept:

A CBDC is something closer to being a perversion of cryptocurrency, or at least of the founding principles and protocols of cryptocurrency—a cryptofascist currency, an evil twin entered into the ledgers on exactly the wrong side, designed to deny its users the basic ownership of their money. | Edward Snowden, whistleblower and privacy advocate

Hyperbole aside, the contrast he’s pointing at is real. A CBDC is state-issued digital fiat, dependent on central bank control and usually on approved intermediaries to hold it. Bitcoin asks permission from no authority, can be held directly by its owner through self-custody, and was built from the start for censorship-resistant, peer-to-peer transfer. A CBDC can be engineered for compliance and control; Bitcoin is engineered to resist both. The two can coexist (one as programmable national money, the other as an apolitical, scarce alternative) but they rest on incompatible philosophies.

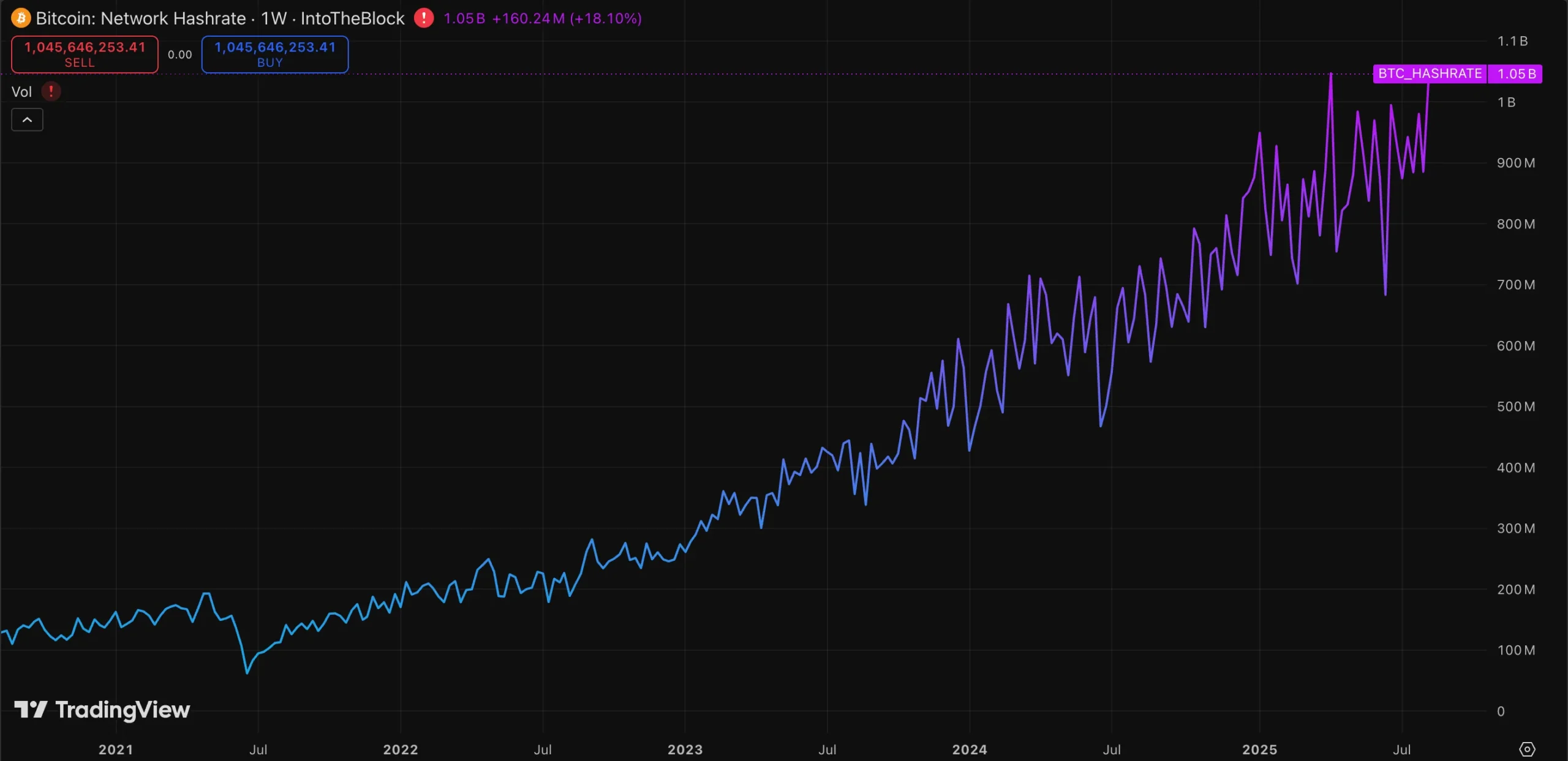

Bitcoin’s censorship resistance rests on something you can measure: the sheer volume of computing power securing the network. That hashrate has climbed almost relentlessly, roughly eightfold since 2021 (Figure 6), distributed across miners worldwide, which is what makes the ledger practically impossible for any single government or company to seize, rewrite or switch off. Where a CBDC’s resistance to censorship is a design choice an issuer can later revoke, Bitcoin’s is a property of its scale and its distribution.

Figure 6. Bitcoin network hashrate, weekly, 2021–2025 | Source: TradingView

Figure 6. Bitcoin network hashrate, weekly, 2021–2025 | Source: TradingView

Could CBDCs Replace Cash or Banks?

QuestionShort answerCould CBDCs replace cash?They could reduce cash use, but most central banks say a CBDC would complement, not replace, cash.Could CBDCs replace banks?Not by design, but they could shrink commercial banks’ role if deposits move into CBDCs.Could CBDCs cause bank runs?They could speed deposit flight in a crisis unless holding limits are built in.Could CBDCs coexist with cash?Yes; most proposals frame them as a complement.Could CBDCs coexist with Bitcoin?Yes; they serve very different purposes.QuestionCould CBDCs replace cash?Short answerThey could reduce cash use, but most central banks say a CBDC would complement, not replace, cash.QuestionCould CBDCs replace banks?Short answerNot by design, but they could shrink commercial banks’ role if deposits move into CBDCs.QuestionCould CBDCs cause bank runs?Short answerThey could speed deposit flight in a crisis unless holding limits are built in.QuestionCould CBDCs coexist with cash?Short answerYes; most proposals frame them as a complement.QuestionCould CBDCs coexist with Bitcoin?Short answerYes; they serve very different purposes.

Officially, central banks are near-unanimous: a CBDC is meant to complement cash, not abolish it, and the ECB has stated flatly that euro banknotes are staying. The real structural risk falls on commercial banks. If households can park money directly at the central bank, they may pull deposits out of private banks, eroding the funding base that supports lending. That is why most retail CBDC proposals include holding caps, limits on how much CBDC any one person can hold, designed specifically to blunt the risk of an accelerated bank run. Bitcoin sits outside this whole argument, since it is not fiat money and is issued by no one.

How fast deposits can actually move is no longer hypothetical. Year-over-year changes in U.S. commercial-bank deposits have swung by trillions of dollars, surging through the 2020–2021 stimulus wave, then turning sharply negative into 2023 as savers chased higher yields and confidence wobbled (Figure 7). A retail CBDC would hand depositors an even faster, frictionless exit straight to the central bank, which is precisely why holding caps appear in nearly every serious proposal.

Figure 7. Change in deposits at all U.S. commercial banks from a year earlier, 1975–2025 | Source: FRED

Figure 7. Change in deposits at all U.S. commercial banks from a year earlier, 1975–2025 | Source: FRED

The Future of CBDCs

A few trends look set to define the next phase:

- Wholesale will win the race: CBDCs used strictly between financial institutions will advance much faster than retail versions, sidestepping public backlash.

- Retail resistance will grow: Public-facing CBDCs will keep struggling with weak adoption and intense political pushback over privacy.

- Cross-border bridges: International projects such as the BIS-linked mBridge and Project Agorá will gain geopolitical weight as countries try to bypass dollar-dominated rails.

- Stablecoins as the competitor: Privately issued stablecoins like USDC and USDT will increasingly compete with CBDCs as the preferred vehicle for everyday digital payments.

- Coexistence over replacement: CBDCs, cash, bank deposits, stablecoins and Bitcoin are likelier to share the field than for any one to wipe out the rest.

Underneath all of it sits one unresolved trade-off: efficiency versus control. The same capabilities that make payments faster can quietly erode privacy and autonomy. As that tension plays out, the appeal of money no government can freeze, inflate at will, or program to expire, money you can actually hold yourself, gets easier to understand. That is the role Bitcoin and self-custody are positioned to play as CBDCs mature.

Closing Thoughts

CBDCs are one of those rare subjects where almost everyone agrees on the facts and almost no one agrees on what they mean. A digital dollar, euro or yuan is, technically, straightforward. The disputes are about power. Strip away the jargon and nearly every argument in this piece collapses into a single question: who controls the money, and on what terms?

The numbers make the dilemma concrete. 137 countries are exploring a CBDC; three have launched a retail version, and even those struggle to get anyone to use it. That gap is the real finding. The engineering was never the hard part, persuading the public to accept money its issuer can see, shape and, in principle, switch off is. Where payment systems already work well, people have little reason to volunteer for that trade; where they don’t, the case is stronger, which is precisely where the live launches happened.

None of this makes a CBDC inherently good or bad. The same programmability that can rush disaster relief to a flooded town can also dictate what a citizen buys and by when. The same ledger that frustrates money launderers can track a dissident. A CBDC is whatever its design makes it, and that design is being drafted right now, largely out of public view, by institutions that don’t agree among themselves on how much privacy to preserve. Which is why the details (holding caps, offline modes, privacy thresholds, who may touch the data) matter far more than the headline.