When you hear that “the Fed raised rates” or “the FOMC held steady,” what does that actually mean? Who decides? Who’s in the room?

The Federal Reserve is the central bank of the United States. The FOMC, or the Federal Open Market Committee, is the committee inside the Fed that makes the interest rate decisions you read about in the news. The two are linked but not the same, and most explainers cover one without the other.

This article covers both: how the Federal Reserve is structured, who serves on its Board, what the FOMC actually does, and how the whole system fits together. The Fed is the main actor in US monetary policy – distinct from fiscal policy, which Congress controls.

What Is the Federal Reserve?

The Federal Reserve, often called “the Fed,” is the central bank of the United States. Created by Congress in 1913 through the Federal Reserve Act (after a series of bank panics in the late 19th and early 20th centuries) it’s responsible for setting monetary policy, supervising banks, maintaining financial-system stability, and providing financial services to banks and the federal government.

The Fed’s two core goals, set by Congress, are usually called the dual mandate: maximum employment and price stability. Price stability is typically interpreted as inflation of around 2% over the long run. These goals can pull against each other (fighting high inflation often means slowing the economy, which can cost jobs) and most Fed decisions involve weighing the trade-off.

The Fed is independent within the government. Its leadership is appointed by the President and confirmed by the Senate, but its day-to-day monetary policy decisions are designed to be insulated from short-term political pressure. The structure lets policy respond to economic data rather than election cycles.

But “the Fed” isn’t a single building or a single committee. It’s a system with three main parts.

The Structure of the Federal Reserve System

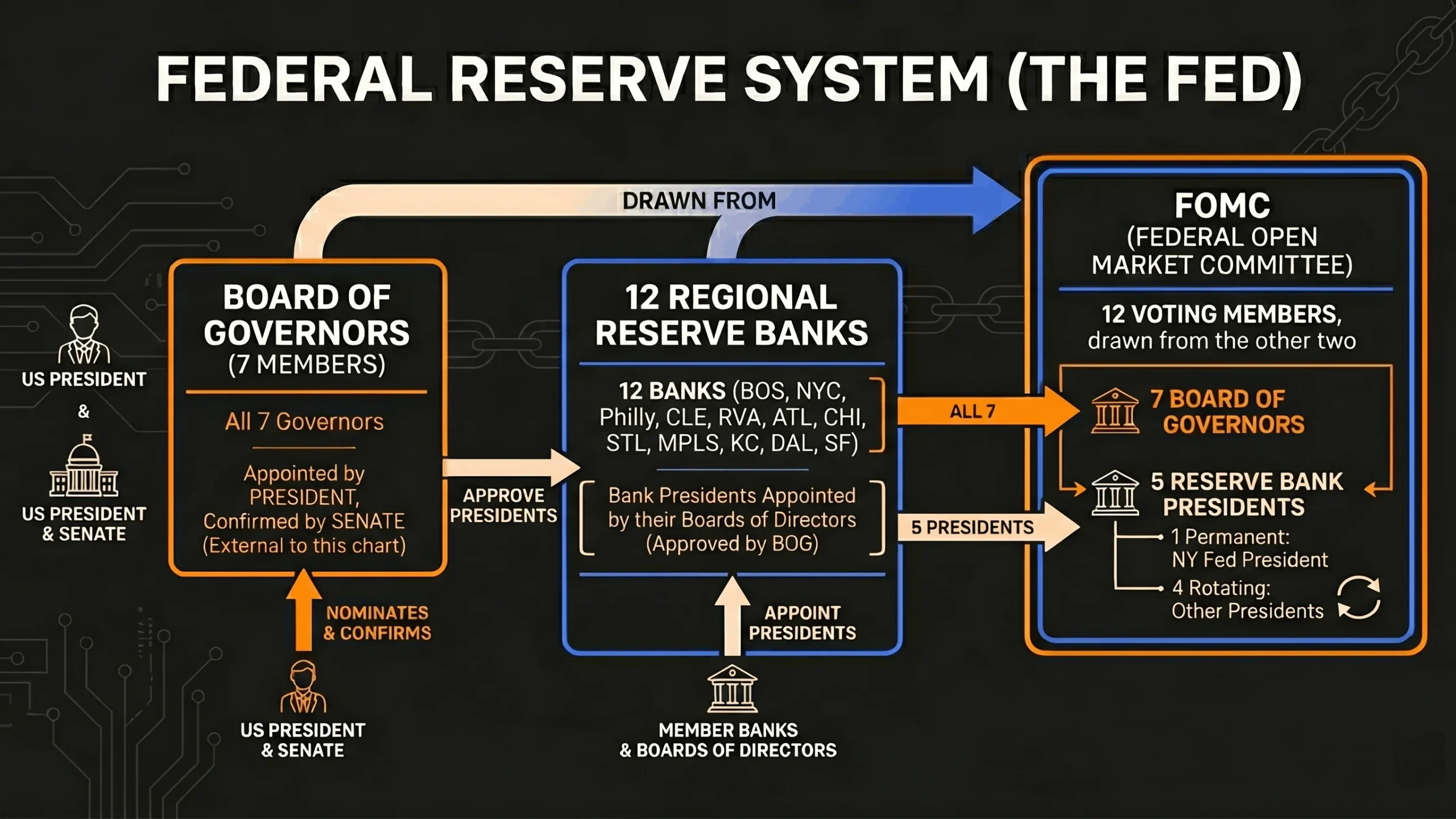

The Federal Reserve System has three connected components: a central board in Washington, twelve regional banks, and a committee that draws from both to set policy.

The Board of Governors

Based in Washington, DC. Seven members, each appointed by the President and confirmed by the Senate to 14-year terms. The terms are staggered so one expires every two years, deliberately spanning multiple administrations. The Board’s chair and vice chair serve 4-year renewable terms in those leadership roles, each requiring separate Senate confirmation. The Board sets the discount rate, oversees the System, and provides most of the FOMC’s voting members.

The 12 regional Federal Reserve Banks

Located in major cities across the country: Boston, New York, Philadelphia, Cleveland, Richmond, Atlanta, Chicago, St. Louis, Minneapolis, Kansas City, Dallas, and San Francisco. Each is led by a president, chosen by its regional board of directors with Board of Governors approval. The regional banks conduct on-the-ground supervision, provide payment services, and contribute economic research that feeds into FOMC discussions.

The Federal Open Market Committee (FOMC)

The committee that actually makes interest rate decisions, drawing members from both the Board and the regional banks. The next section covers it in detail.

The three components are deliberately overlapping. The Board appoints public-interest directors at regional banks; the regional banks contribute presidents to the FOMC; the FOMC sets policy that the system implements.

What Is the FOMC and What Does It Decide?

The Federal Open Market Committee (FOMC) is the committee within the Federal Reserve that sets US monetary policy. It’s best known for its decisions on the federal funds rate — the benchmark interest rate that influences almost every other rate in the US economy.

The FOMC has 12 voting members:

- All 7 members of the Board of Governors

- The president of the New York Fed, who holds a permanent vote (the New York Fed conducts the Fed’s open market operations)

- 4 of the remaining 11 regional Fed presidents, rotating annually

The four rotating seats are filled from four geographic groupings, one president per group. All 12 regional presidents attend FOMC meetings and participate in the discussion; they just don’t all vote in the same year. For 2026, the rotating voters are the presidents of the Cleveland (Beth Hammack), Dallas (Lorie Logan), Philadelphia (Anna Paulson), and Minneapolis (Neel Kashkari) Reserve Banks.

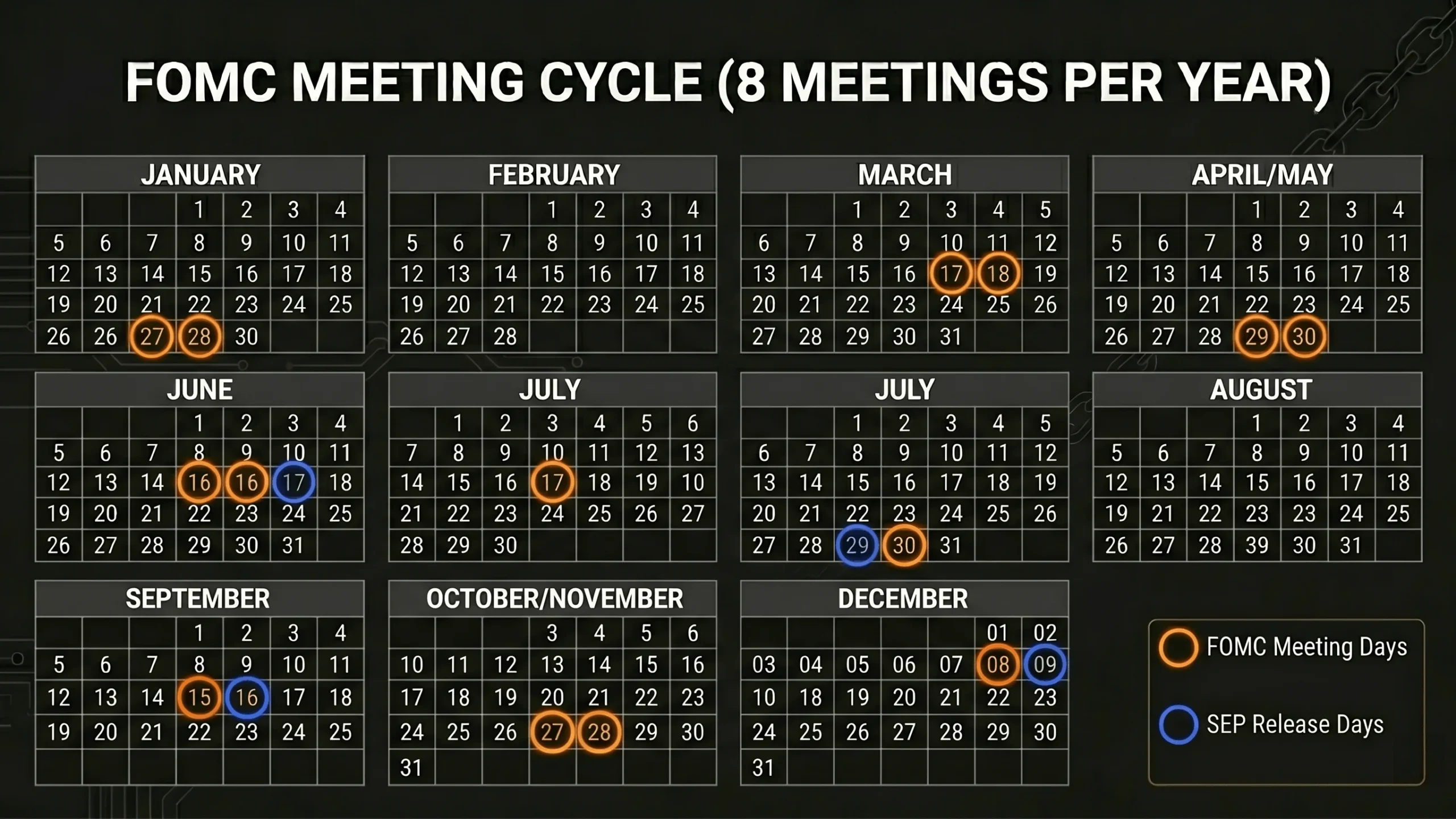

The FOMC meets 8 times a year, roughly every six weeks. Each meeting produces a written policy statement; four of the eight also include an updated Summary of Economic Projections (SEP) – the “dot plot” showing where individual members see rates heading. After each meeting, the chair holds a press conference.

At each meeting, the FOMC decides the target range for the federal funds rate, the pace of any balance sheet operations, and the forward guidance in the official statement, which markets parse word by word. When financial news refers to “a Fed decision” or “a rate cut,” it almost always means an FOMC decision. As of late May 2026, the target range sits at 3.5%–3.75%, following a hold at the April 29 meeting.

The Fed’s Main Tools and How Decisions Affect You

The Fed has a small toolkit, but each tool has wide reach.

The federal funds rate is the headline tool. The Fed sets a target range, then uses open market operations and interest paid on bank reserves to keep the market rate inside it. Changes ripple outward to mortgage rates, credit card APRs, savings yields, business loan rates, and the cost of government borrowing.

Quantitative easing (QE) and quantitative tightening (QT) are the balance sheet tools. QE adds money to the system by buying bonds; QT pulls it back out by letting bonds mature without replacement.

Interest on reserves is the rate the Fed pays banks for funds parked at the Fed. It sets a floor that helps keep the federal funds rate where the Fed wants it.

The discount rate is what the Fed charges banks for direct short-term loans through the “discount window.” Used relatively rarely but important in stressed funding conditions.

Forward guidance, the FOMC’s communication about likely future policy, is often the most impactful tool. Markets price in expected rate changes long before they happen, so a well-chosen sentence in an FOMC statement can move financial conditions before any rate actually moves.

If you have a mortgage, a credit card, a savings account, or a job, Fed decisions affect you – usually indirectly, through what banks and businesses do in response.

Who Runs the Fed? Leadership and Appointments

Current as of May 25, 2026. The Fed’s Board composition changes; see federalreserve.gov for the live roster.

The Chair of the Federal Reserve is the most visible figure at the Fed. The chair leads both the Board and the FOMC, holds the post-meeting press conferences, and is the public face of US monetary policy. The chair is appointed by the President and confirmed by the Senate for a 4-year renewable term, separate from the underlying 14-year governor seat.

Kevin Warsh is serving as Chair. He was confirmed by the Senate on May 13, 2026, and succeeded Jerome Powell when Powell’s term as chair ended on May 15. Warsh previously served as a Federal Reserve governor; his underlying Board seat now runs until 2040.

Powell remains on the Board as a governor. His underlying governor term runs through January 2028, and he has indicated he intends to stay on the Board until the resolution of an ongoing investigation related to the Federal Reserve’s headquarters renovation. The last time a former Fed chair returned to the Board after stepping down was nearly 80 years ago.

The seven current governors are Kevin Warsh (Chair), Philip Jefferson (Vice Chair, term ends 2027), Michelle Bowman (Vice Chair for Supervision, term ends 2029), Michael Barr, Lisa Cook, Christopher Waller, and Jerome Powell.

Appointments: governors are nominated by the President and confirmed by the Senate. Regional Fed presidents are chosen by their regional boards and approved by the Board of Governors. The split, political appointment at the top, regional selection at the regional banks, is part of how the Fed balances democratic accountability with operational independence.

Conclusion

The next time you see a headline about a Fed rate cut, a chair confirmation, or an inflation report, you can map it onto the actual structure: a seven-member Board, twelve regional banks, and a twelve-member FOMC drawing from both. The Fed is designed to be independent in its day-to-day decisions while remaining politically accountable in the long run. It will keep making news. Knowing how it’s built is the difference between watching that news and understanding it.