When you hear that “the Fed is buying bonds” or that “the Fed is shrinking its balance sheet,” that’s quantitative easing or quantitative tightening: two of the most powerful tools modern central banks have. Both have been used heavily in the last 15 years, and both shape interest rates, asset prices, and the economy you live in.

The basic idea is straightforward. Quantitative easing (QE) adds money to the financial system by having the central bank buy bonds. Quantitative tightening (QT) pulls money back out by letting those bonds mature or selling them.

They’re two directions of the same lever, and they typically run alongside interest rate decisions as part of broader monetary policy, which is different from fiscal policy in important ways. This article covers how each one actually works, why central banks use them, how they compare, and where the Fed is right now.

What Is Quantitative Easing (QE)?

Quantitative easing (QE) is when a central bank creates new reserves to buy large amounts of bonds, usually government bonds and mortgage-backed securities, in order to push down long-term interest rates and inject money into the financial system.

QE is used by the world’s major central banks, including the Federal Reserve in the US, the European Central Bank (ECB), the Bank of England, and the Bank of Japan. The BOJ was the first to deploy modern QE, in 2001; the Fed followed in late 2008.

Mechanically, here’s how quantitative easing works:

- The central bank creates new bank reserves digitally, not physical currency.

- It uses those reserves to buy bonds from large financial institutions.

- The institutions now hold cash instead of bonds, so they have more to lend.

- Increased demand for bonds pushes bond prices up and long-term yields down, making it cheaper to borrow for mortgages, business loans, and corporate debt.

Central banks typically reach for QE when the short-term policy rate is already near zero and the central bank wants to provide more stimulus than rate cuts alone can deliver. The short version: QE expands the central bank’s balance sheet to push more money into the economy when cutting rates isn’t enough.

What Is Quantitative Tightening (QT)?

Quantitative tightening (QT) is the opposite of QE. The central bank reduces the size of its balance sheet by letting bonds mature without reinvesting the proceeds, or by actively selling them. This pulls money out of the financial system.

There are two ways to run QT:

- Passive QT lets maturing bonds “roll off” the balance sheet without buying replacements. The Fed gets paid back; the cash effectively disappears from circulation. This is the approach the Fed has used in both of its QT cycles.

- Active QT has the central bank directly sell bonds back into the market. It’s much rarer in practice, as selling at scale risks destabilizing bond markets, so central banks generally prefer the slower, gentler passive approach.

Central banks use QT for three main reasons. First, to reduce the money supply and help cool inflation. Second, to normalize the balance sheet after a period of QE, shrinking it back toward something closer to pre-crisis size. Third, to rebuild policy room – a smaller balance sheet means more capacity to expand again in the next crisis without entering uncharted territory.

The practical effect of QT tends to mirror QE in reverse: it pushes long-term interest rates up and reduces financial-system liquidity, complementing rate hikes when the central bank is trying to tighten policy.

QE vs QT: How They Compare

XQuantitative Easing (QE)Quantitative Tightening (QT)DirectionAdds money to the financial systemRemoves money from the financial systemMechanismCentral bank buys bondsCentral bank lets bonds mature or sells themEffect on balance sheetExpands itShrinks itEffect on long-term ratesPushes rates downPushes rates upTypical economic contextRecession or crisisRecovery or inflationGoalStimulate borrowing and growthCool the economy, normalize policyCommon paceAggressive when usedSlower and more cautiousXDirectionQuantitative Easing (QE)Adds money to the financial systemQuantitative Tightening (QT)Removes money from the financial systemXMechanismQuantitative Easing (QE)Central bank buys bondsQuantitative Tightening (QT)Central bank lets bonds mature or sells themXEffect on balance sheetQuantitative Easing (QE)Expands itQuantitative Tightening (QT)Shrinks itXEffect on long-term ratesQuantitative Easing (QE)Pushes rates downQuantitative Tightening (QT)Pushes rates upXTypical economic contextQuantitative Easing (QE)Recession or crisisQuantitative Tightening (QT)Recovery or inflationXGoalQuantitative Easing (QE)Stimulate borrowing and growthQuantitative Tightening (QT)Cool the economy, normalize policyXCommon paceQuantitative Easing (QE)Aggressive when usedQuantitative Tightening (QT)Slower and more cautious

Three nuances are worth understanding beyond the table.

QE and QT aren’t perfectly symmetric. QE has been deployed at large scale and at speed, the Fed’s balance sheet roughly doubled in months in 2020. QT has been more cautious; central banks worry that pulling liquidity too fast breaks things in funding markets.

Both work through bond markets, not the short-term policy rate. The federal funds rate directly affects overnight lending between banks. QE and QT work on the long end of the yield curve — mortgage rates, corporate bond yields, 10-year Treasuries.

They typically run alongside rate decisions rather than instead of them. The Fed can raise rates and run QT at the same time, as it did from 2022 through 2025, for a compounded tightening effect. Likewise, rate cuts plus QE work in the same direction.

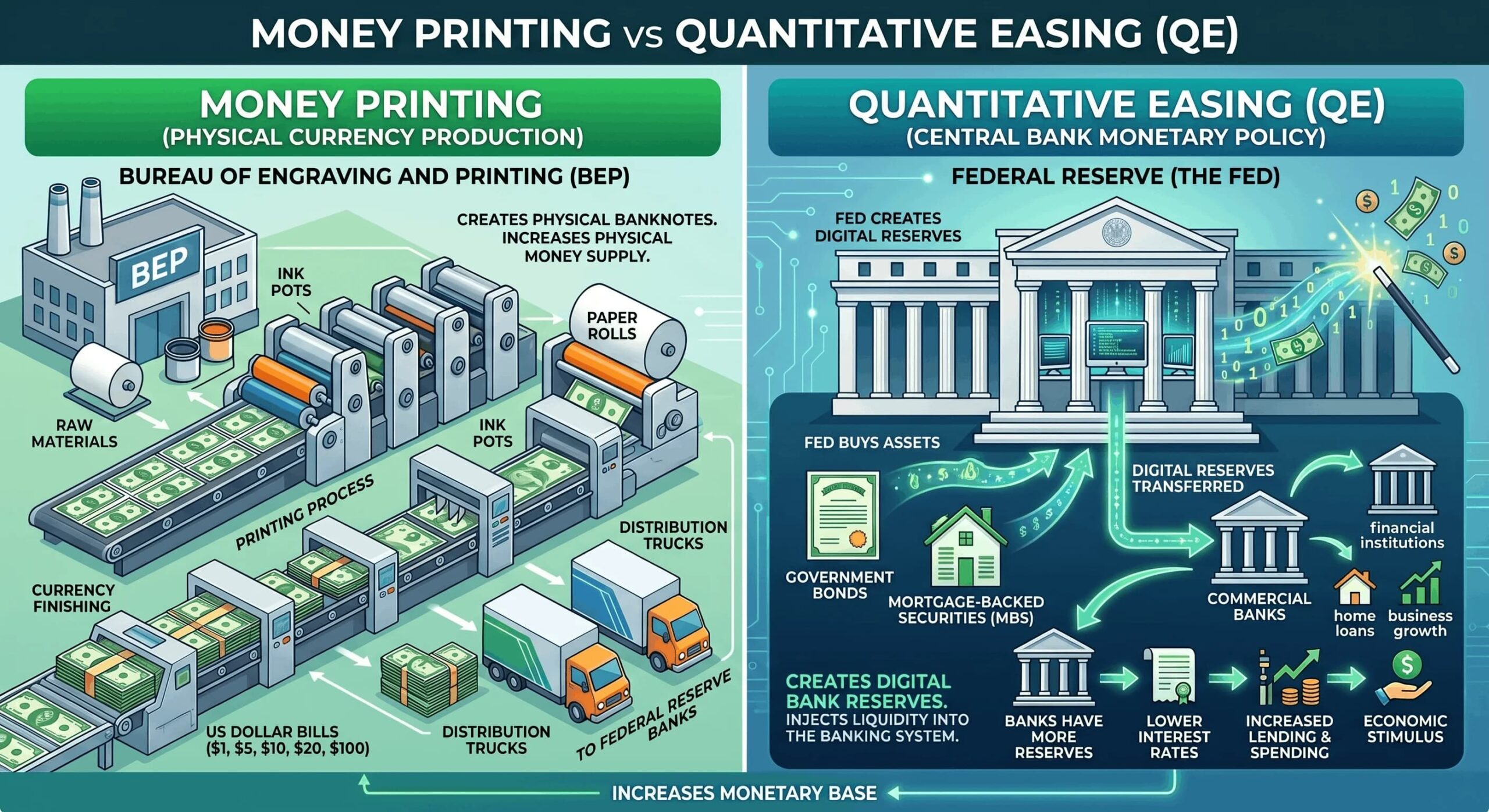

Is QE Just “Money Printing”?

QE is often described, including in financial headlines, as “money printing.” That’s a useful shorthand, but it’s not technically correct, and the distinction matters.

Literal money printing is the physical production of currency by the Bureau of Engraving and Printing. It’s done to replace worn-out bills in circulation, not to expand the money supply. The currency in your wallet doesn’t multiply when the Fed does QE.

What QE actually creates is new bank reserves – electronic balances that commercial banks hold at the Fed. Those reserves can flow into the broader money supply when banks lend them out, but they don’t have to. Through much of the post-2008 QE era, banks held large amounts of “excess reserves” parked at the Fed rather than lending them aggressively. The Fed’s balance sheet grew enormously; the broader money supply grew much less.

The cleanest way to think about it: QE creates digital reserves; printing money creates paper bills. Both can increase the money supply in some sense, but the mechanisms are different — and the assumption that QE automatically produces inflation rests on this conflation more than on the evidence.

QE and QT in Recent History

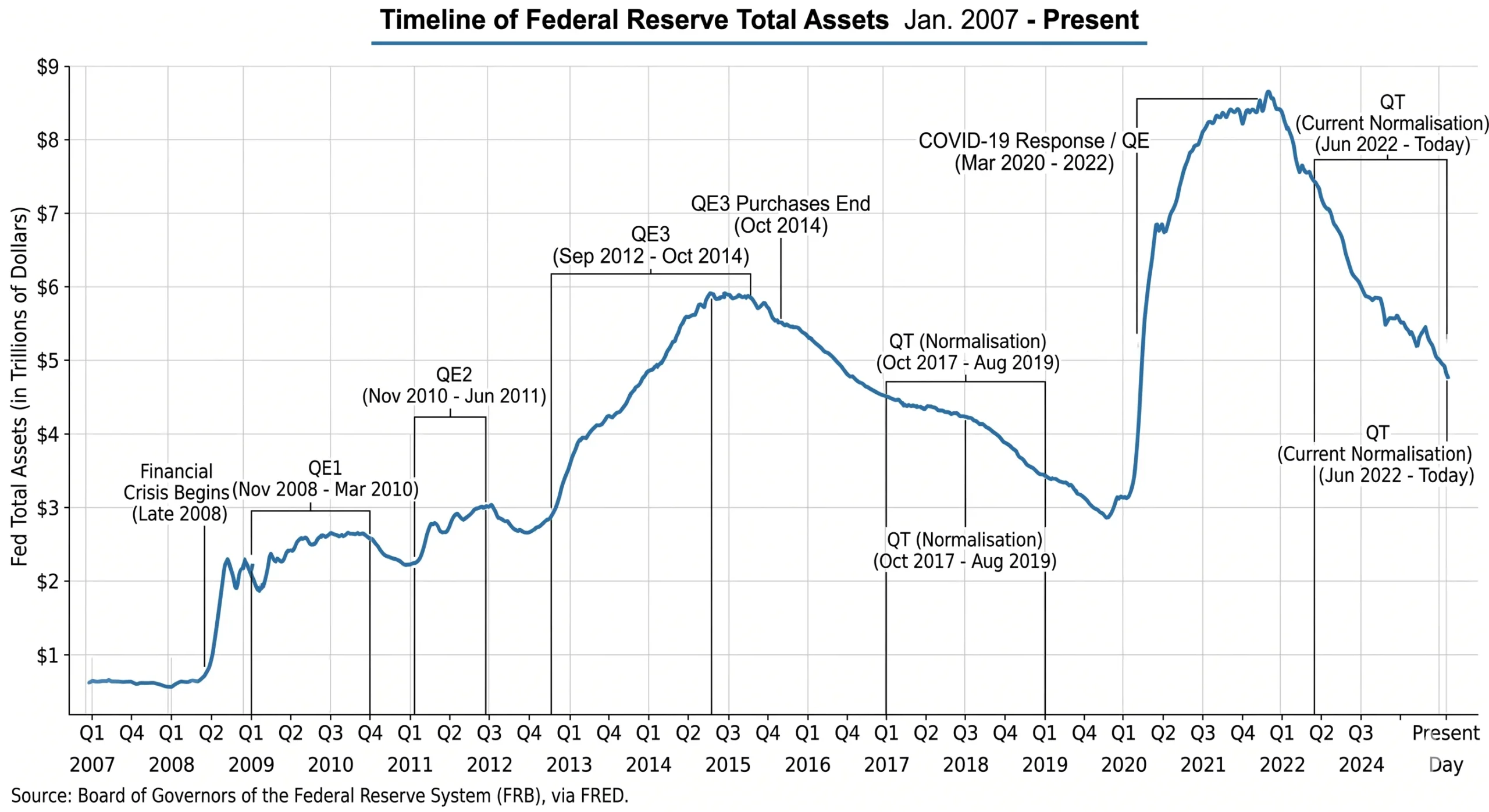

The last 17 years contain the entire modern history of QE and QT. Five episodes cover almost all of it.

The original QE rounds (2008–2014)

The Fed launched QE1 in late 2008 in response to the global financial crisis, followed by QE2 in 2010 and QE3 from 2012 to 2014. The balance sheet grew from roughly $900 billion in mid-2008 to about $4.5 trillion by late 2014. This was the first US deployment of QE, and at the time, the scale was unprecedented.

The first QT cycle (2017–2019)

After three years of holding the balance sheet steady, the Fed began letting bonds roll off in October 2017. The cycle ended abruptly in 2019 after liquidity strains in short-term funding markets forced the Fed to start growing reserves again. The balance sheet bottomed at roughly $3.8 trillion before turning back up.

The COVID-19 expansion (2020–2022)

In response to the pandemic, the Fed restarted QE at unprecedented scale, buying Treasuries and mortgage-backed securities at a pace that took the balance sheet from $4.2 trillion in February 2020 to a peak of about $8.9 trillion in April 2022.

The 2022–2025 QT cycle

The Fed began QT in June 2022, letting bonds roll off the balance sheet alongside its aggressive rate-hiking cycle. The pace accelerated through 2023 and continued into 2025. It was the most coordinated tightening in decades.

Current state (post-December 2025)

The Fed announced the end of QT at its October 2025 meeting, and the program formally concluded on December 1, 2025. The balance sheet stabilized at roughly $6.57 trillion, well above pre-pandemic levels but down meaningfully from the 2022 peak. The Fed has signaled it will now run “reserve management” operations, reinvesting maturing securities to keep the balance sheet roughly flat. For current figures, see the Fed’s balance sheet page.

Conclusion

What started in 2008 as an emergency response is now a standard part of how central banks operate. The Fed has gone through two complete QT cycles in less than a decade, and the most recent one left the balance sheet at roughly $6.5 trillion, far above pre-2008 levels but well below the pandemic peak. When you read that the Fed is “tightening” or “easing,” the rate decision is only half the story. The balance sheet is the other half, and now you know how to read it.