A US $100 bill costs the government about 17 cents to print. Yet hand one to a stranger and they’ll give you a hundred dollars’ worth of real goods in return: groceries, a tank of fuel, a night in a hotel. The paper is nearly worthless; the agreement it represents is not. That gap between an object’s physical cost and its accepted value is the central mystery of money, and unpacking it explains almost everything about how modern economies work.

This guide covers what money does, what makes something good at being money, the forms it has taken across history, and where it’s heading as cash goes digital. No economics background required. In short, money is anything widely accepted as a medium of exchange, a store of value, and a unit of account. It lets people trade without barter, measure every price on one common scale, and store purchasing power to spend later.

Key Takeaways

- Money is valuable because people accept it, not because of the material it is made from.

- Economists define money by what it does: medium of exchange, unit of account, and store of value.

- Good money tends to be durable, portable, divisible, uniform, scarce, and widely accepted.

- Modern fiat currencies are not backed by gold or silver; they rely on trust, government authority, and economic acceptance.

- Most money today exists digitally as bank deposits rather than physical cash.

- The future of money is being shaped by stablecoins, central bank digital currencies (CBDCs), cryptocurrencies like Bitcoin, and the decline of physical cash.

Simple version: Money is a shared belief system with practical rules. It works because people expect other people to accept it.

What Is Money? The Simple Definition

Money is a shared tool for settling debts and trading value. Its power comes not from any law of nature but from collective agreement: a thing is money because enough people treat it as money. Adam Smith caught this in The Wealth of Nations (1776), calling money the “great wheel of circulation.” It’s the mechanism that keeps goods moving through an economy without ever being consumed itself.

Just how far that agreement can stretch is clear from the Pacific island of Yap, where wealth long took the form of rai: limestone discs, some twelve feet across and far too heavy to move. Ownership passed by word of mouth while the stone stayed put, and when one famous disc reportedly sank to the seabed during transport, everyone agreed it was still owned, still spendable, still money. If that sounds absurd, most of your own money is just numbers in a database you’ll never see.

Two words get used interchangeably but shouldn’t. Money is the broad concept, the social technology for storing and exchanging value. Currency is a specific form it takes: dollars, euros, yen, the coins in your pocket. All currency is money, but money is bigger than any one currency. This is the distinction that matters the moment you compare dollars to gold, or fiat to Bitcoin.

Money vs currency

The easiest way to separate the terms is to distinguish the thing being valued from the form, system, or record used to represent and move it.

TermMeaningExampleKey distinctionMoneyThe broad social technology for storing and exchanging valueDollars, gold, Bitcoin, bank depositsThe concept itselfCurrencyA specific form money takesDollar bills, euros, yenA representation of moneyPayment railThe system that moves moneyVisa, ACH, SWIFT, FedNowInfrastructure, not moneyAccount balanceA record of money owed to youBank account, Venmo balanceA ledger entryAssetSomething valuable that may not function as moneyStocks, real estate, artNot necessarily spendableTermMoneyMeaningThe broad social technology for storing and exchanging valueExampleDollars, gold, Bitcoin, bank depositsKey distinctionThe concept itselfTermCurrencyMeaningA specific form money takesExampleDollar bills, euros, yenKey distinctionA representation of moneyTermPayment railMeaningThe system that moves moneyExampleVisa, ACH, SWIFT, FedNowKey distinctionInfrastructure, not moneyTermAccount balanceMeaningA record of money owed to youExampleBank account, Venmo balanceKey distinctionA ledger entryTermAssetMeaningSomething valuable that may not function as moneyExampleStocks, real estate, artKey distinctionNot necessarily spendable

So what gives money its value? Three things working together: acceptability (others will take it in trade), trust (you believe it’ll still be accepted tomorrow), and scarcity (it can’t be created without limit). Remove any one and money starts to fail, exactly what history shows.

The 3 Functions of Money

Economists define money by what it does, not what it’s made of. The three core functions are a medium of exchange, a unit of account, and a store of value; anything that performs all three reliably is money. (Some add a fourth, below.)

Medium of exchange

Money’s headline job: it sits in the middle of every transaction so you never swap goods directly for other goods. Without it you’re stuck with barter, which only works if the person who has what you want also wants what you have. This is known as the double coincidence of wants, a coincidence so rare it strangles trade.

The economist William Stanley Jevons illustrated it with a true story. In the 1860s the French singer Mademoiselle Zélie gave a concert in the Society Islands and was paid her fee, a third of the receipts, in three pigs, twenty-three turkeys, forty-four chickens, five thousand coconuts, and heaps of bananas, lemons, and oranges.

In Paris it would have been a small fortune; on the island she couldn’t eat it all, so she ended up feeding the fruit to the pigs and poultry just to keep her earnings alive. Money dissolves that problem: everyone accepts it, so everyone can buy from anyone.

Unit of account

Money gives an economy one yardstick for value. A coffee costs $4; a bicycle costs $400. Priced in the same unit, you see instantly that the bicycle is worth a hundred coffees. Try pricing that coffee in eggs, haircuts, and bus rides at once and the chaos is obvious. A common unit of account is what lets accounting, contracts, wages, and taxes exist at all.

Store of value

Money lets you sell something today and buy something else years from now, because it holds purchasing power across time. A perfect currency would buy the same basket of goods in a decade as it does today. Inflation steadily erodes this, which is why store of value is the function modern money struggles with most.

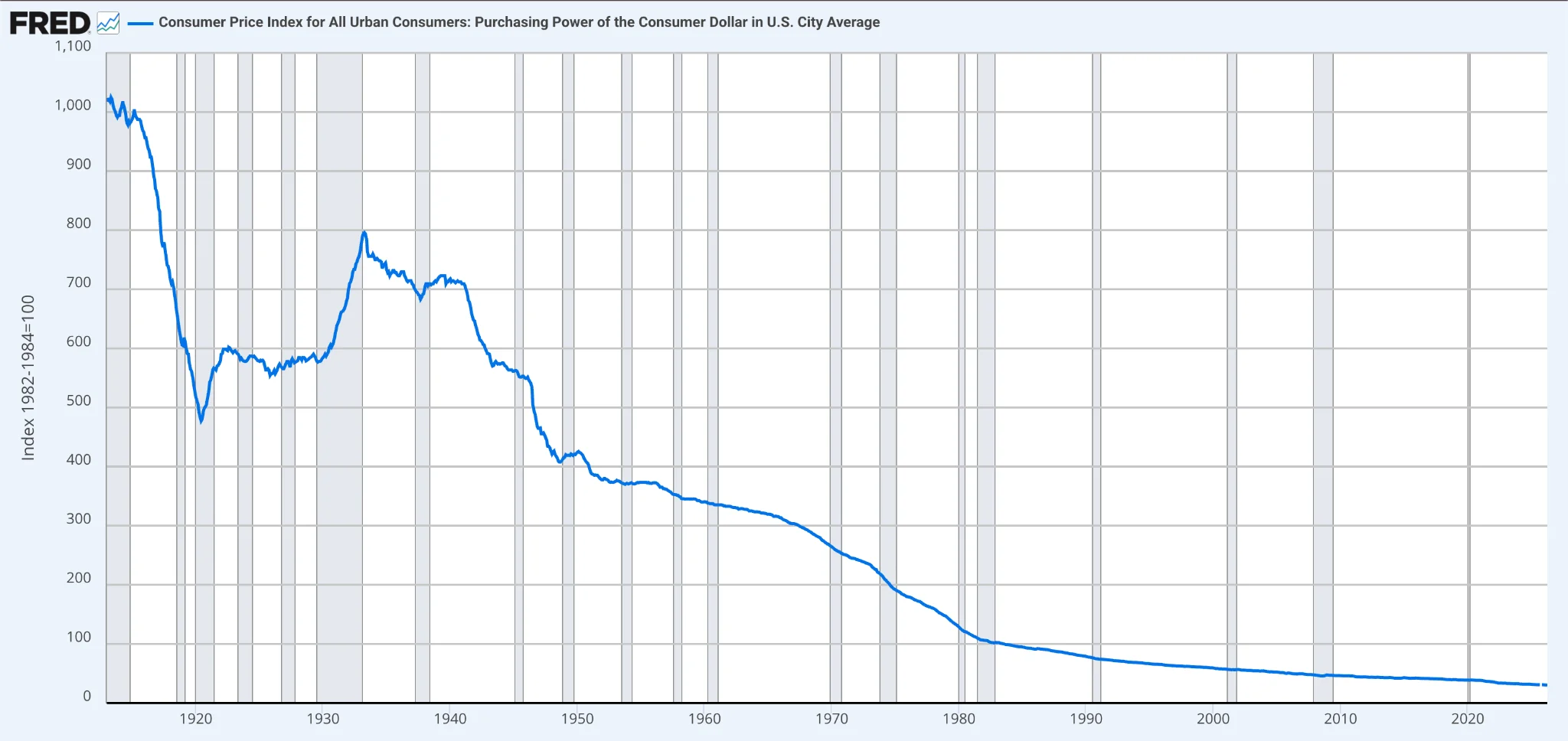

The dollar’s purchasing power has fallen dramatically since the creation of the Federal Reserve, showing why the store-of-value function is the hardest job for modern money.

The dollar’s purchasing power has fallen dramatically since the creation of the Federal Reserve, showing why the store-of-value function is the hardest job for modern money.

Standard of deferred payment: the fourth function

Some economists add a fourth function: money as the standard unit in which debts are denominated and repaid over time. A loan or multi-year contract fixes the obligation in money, which only works if the currency’s value stays reasonably stable between the day the debt is created and the day it comes due. Another reason stability matters.

The Properties of Good Money

Across thousands of years and wildly different cultures, the things that endured as money shared the same handful of traits. A Picasso may be valuable, but it’s hard to divide, hard to price consistently, and impossible to spend at the grocery store. Money succeeds when it moves value efficiently across people, places, and time. The six properties:

- Durability: it survives repeated handling and the passage of time without rotting, rusting, or falling apart.

- Portability: it packs a lot of value into a small, transferable form, so you can move it without a cart.

- Divisibility: it splits cleanly into smaller units, such as dollars into cents, without losing value, for both large and tiny transactions.

- Uniformity, or fungibility: every unit is interchangeable; one dollar is exactly as good as any other.

- Limited supply, or scarcity: it can’t be produced at will, which protects holders from debasement, the slow dilution of value when more is created.

- Acceptability: enough people recognise and accept it that you can reliably spend it.

Money that scores well on all six is what advocates call sound money or hard money: hard to produce, and therefore good at holding its value. Its opposite, soft money, is easy to create and prone to losing purchasing power; that tension is the hard money vs soft money debate. Gold earned its monetary status by scoring high on most of these traits for millennia; Bitcoin is the newest contender, argued to score well on scarcity, portability, and divisibility.

Hard money vs soft money

The core difference is whether supply is difficult to expand or easy to expand, which affects how well money preserves purchasing power over time.

FeatureHard moneySoft moneySupply growthDifficultEasyExamplesGold, BitcoinFiat currenciesMain benefitProtects purchasing powerFlexible during crisesMain riskCan be rigid or volatileInflation and debasementSupporters valueScarcityEconomic flexibilityFeatureSupply growthHard moneyDifficultSoft moneyEasyFeatureExamplesHard moneyGold, BitcoinSoft moneyFiat currenciesFeatureMain benefitHard moneyProtects purchasing powerSoft moneyFlexible during crisesFeatureMain riskHard moneyCan be rigid or volatileSoft moneyInflation and debasementFeatureSupporters valueHard moneyScarcitySoft moneyEconomic flexibility

Reader takeaway: The best money isn’t the thing with the most intrinsic value. It’s the thing that most reliably transfers value through time.

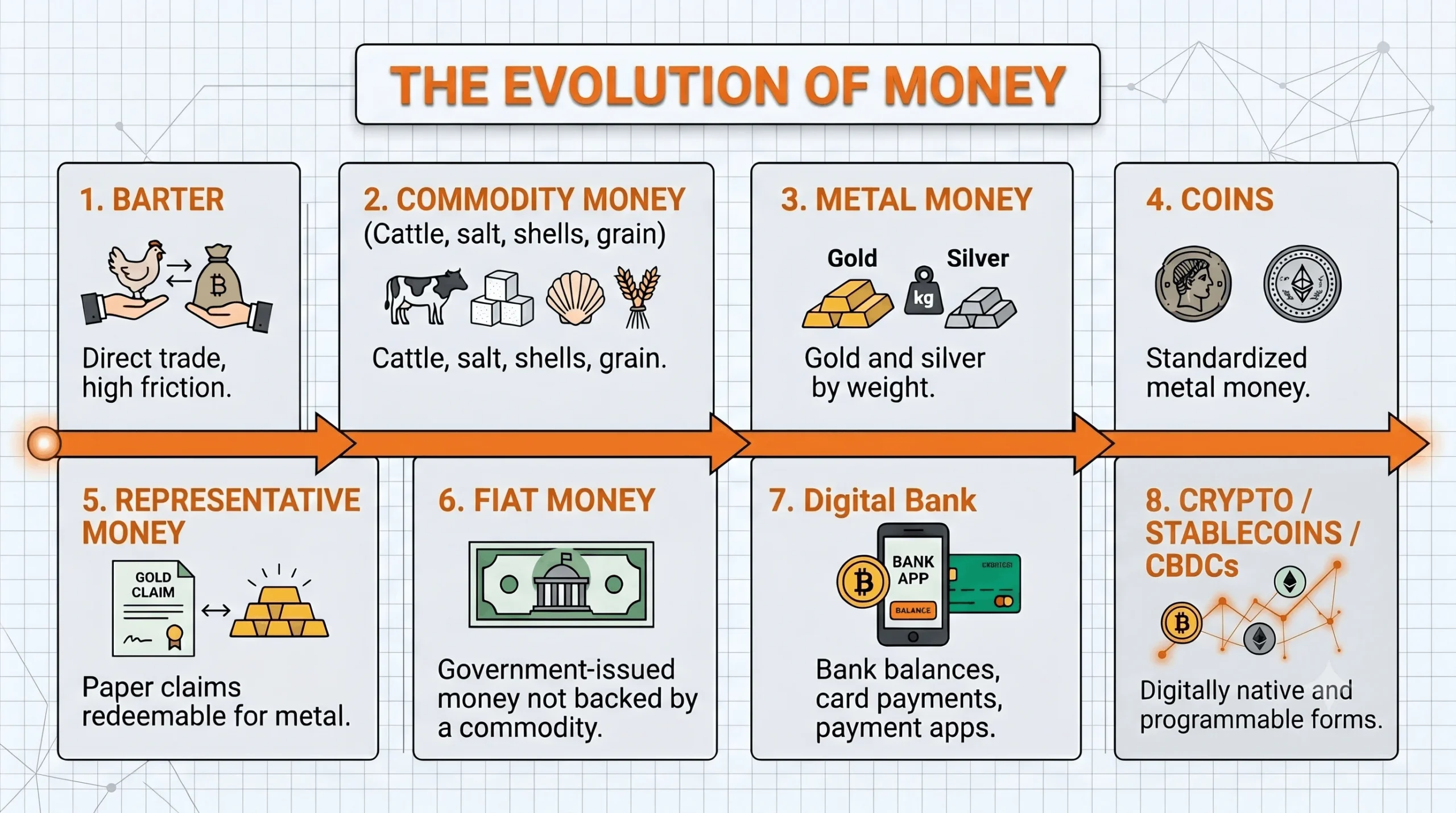

A Brief History of Money

Money wasn’t invented in a single moment. It evolved, repeatedly, as societies outgrew whatever they were using before. It begins with the limits of barter. Picture a shoemaker who wants grain: he must find a farmer who has surplus grain and happens to need shoes, that double coincidence again. If the farmer wants a knife instead, the trade collapses, and barter economies stay small because the friction of matching needs is enormous.

The first fix was commodity money: a widely desired good everyone accepts, even if they don’t want it for its own sake. Societies landed on cattle, salt, cowrie shells, and grain; over time metals won out, and gold and silver won among metals, because they were durable, divisible, portable, and naturally scarce.

The earliest known standardised coins were struck from electrum, a natural gold-silver alloy, in the kingdom of Lydia (modern-day Turkey) around 600 BCE, as documented by the British Museum and the historian Herodotus. So who invented money? There’s no single inventor, but Lydia gives us the first coinage we can point to.

Carrying chests of metal was risky, so next came representative money: paper claims redeemable for a fixed amount of metal held in a vault. Chinese merchants used notes called jiaozi as early as the Song dynasty, and European goldsmiths issued receipts for deposited gold that began circulating as money in their own right. The paper had no value itself; its worth was whatever it could be exchanged for.

The final leap was fiat money, backed by no commodity, valuable only because a government declares it so and the public trusts it. The modern fiat era was sealed in stages: the 1944 Bretton Woods system tied world currencies to a US dollar that was itself convertible to gold, and in 1971 President Nixon suspended that convertibility, ending the gold standard. Since then nothing physical backs the dollar. So what does? Government decree, the requirement to pay taxes in it, and collective faith .

Types of Money

Today’s money comes in several types, each drawing its value from a different source.

TypeSource of valueExampleStrengthWeaknessCommodity moneyMaterial itselfGoldScarcityDifficult to transportRepresentative moneyRedeemable promiseGold-backed notesConvenientRequires trustFiat moneyGovernment authorityUS dollarFlexibleInflation riskBank moneyCommercial bank depositsChecking accountConvenientDepends on banking systemCryptocurrencyNetwork rulesBitcoinDecentralizedVolatileStablecoinPegged reservesUSDCStable digital paymentsIssuer riskCBDCCentral bank liabilityDigital yuanState-backedPrivacy concernsTypeCommodity moneySource of valueMaterial itselfExampleGoldStrengthScarcityWeaknessDifficult to transportTypeRepresentative moneySource of valueRedeemable promiseExampleGold-backed notesStrengthConvenientWeaknessRequires trustTypeFiat moneySource of valueGovernment authorityExampleUS dollarStrengthFlexibleWeaknessInflation riskTypeBank moneySource of valueCommercial bank depositsExampleChecking accountStrengthConvenientWeaknessDepends on banking systemTypeCryptocurrencySource of valueNetwork rulesExampleBitcoinStrengthDecentralizedWeaknessVolatileTypeStablecoinSource of valuePegged reservesExampleUSDCStrengthStable digital paymentsWeaknessIssuer riskTypeCBDCSource of valueCentral bank liabilityExampleDigital yuanStrengthState-backedWeaknessPrivacy concerns

Commodity money is valuable for what it’s made of: the gold in a coin is worth something even melted down. Representative money is valuable for what it can be redeemed for: a gold-backed note is just paper, but the promise of metal behind it is where its worth lives.

Fiat money is valuable because a government decrees it legal and the public trusts it; that’s the fiat money definition in a sentence, and it describes every banknote in your wallet. Its great strength, supply managed by a central bank, is also its great weakness, since that supply can expand and dilute purchasing power through inflation.

Legal tender is a narrower idea: money the law requires creditors to accept in settlement of debts. Dollars are legal tender in the United States, so you can’t be refused them when paying off a debt.

Digital and electronic money is the fastest-growing category, and it splits in two. Most is digitised fiat, the same dollars and euros, represented as numbers in a bank database, a Venmo balance, or a card swipe rather than physical cash.

Modern Money and Its Problems

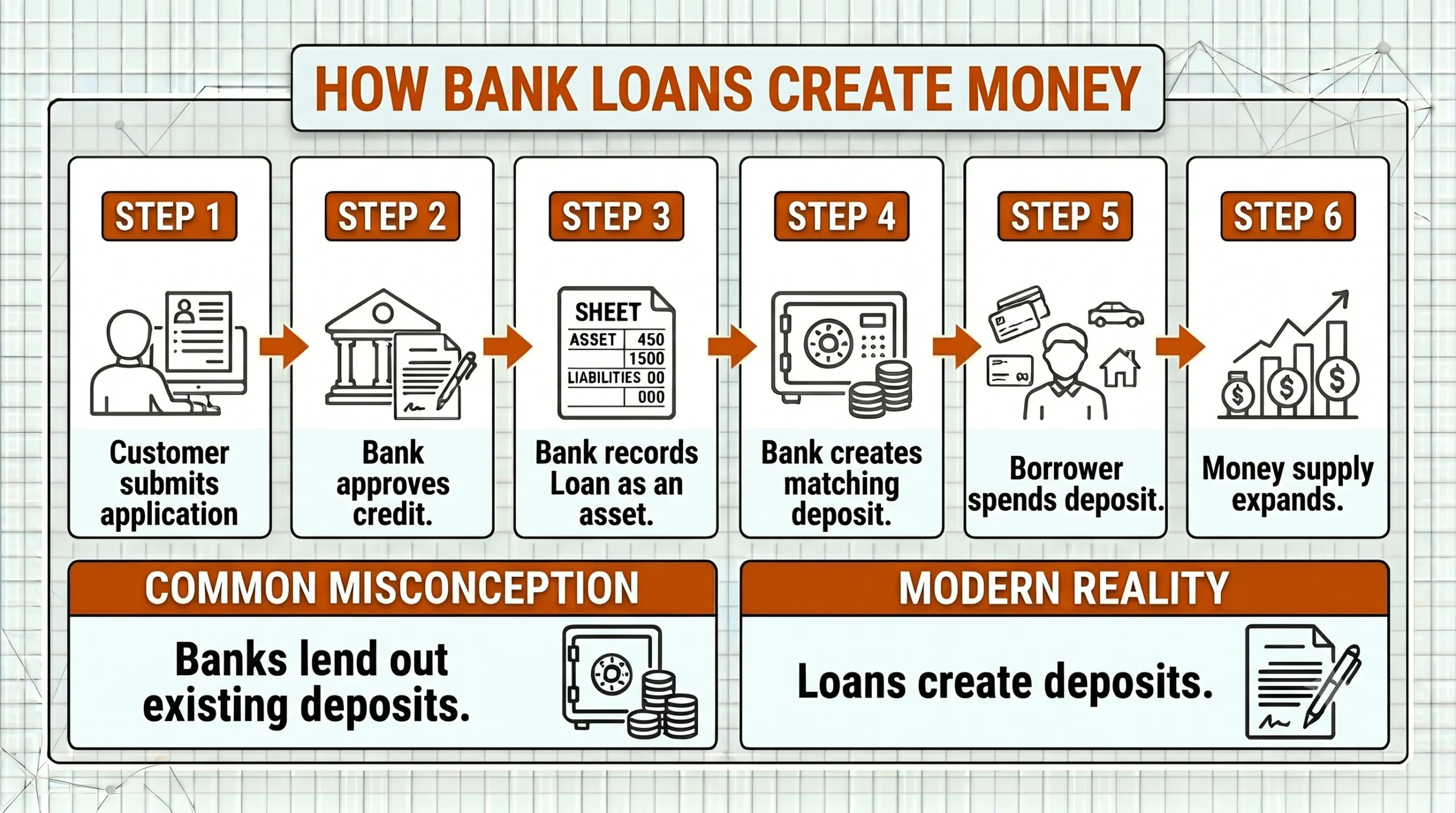

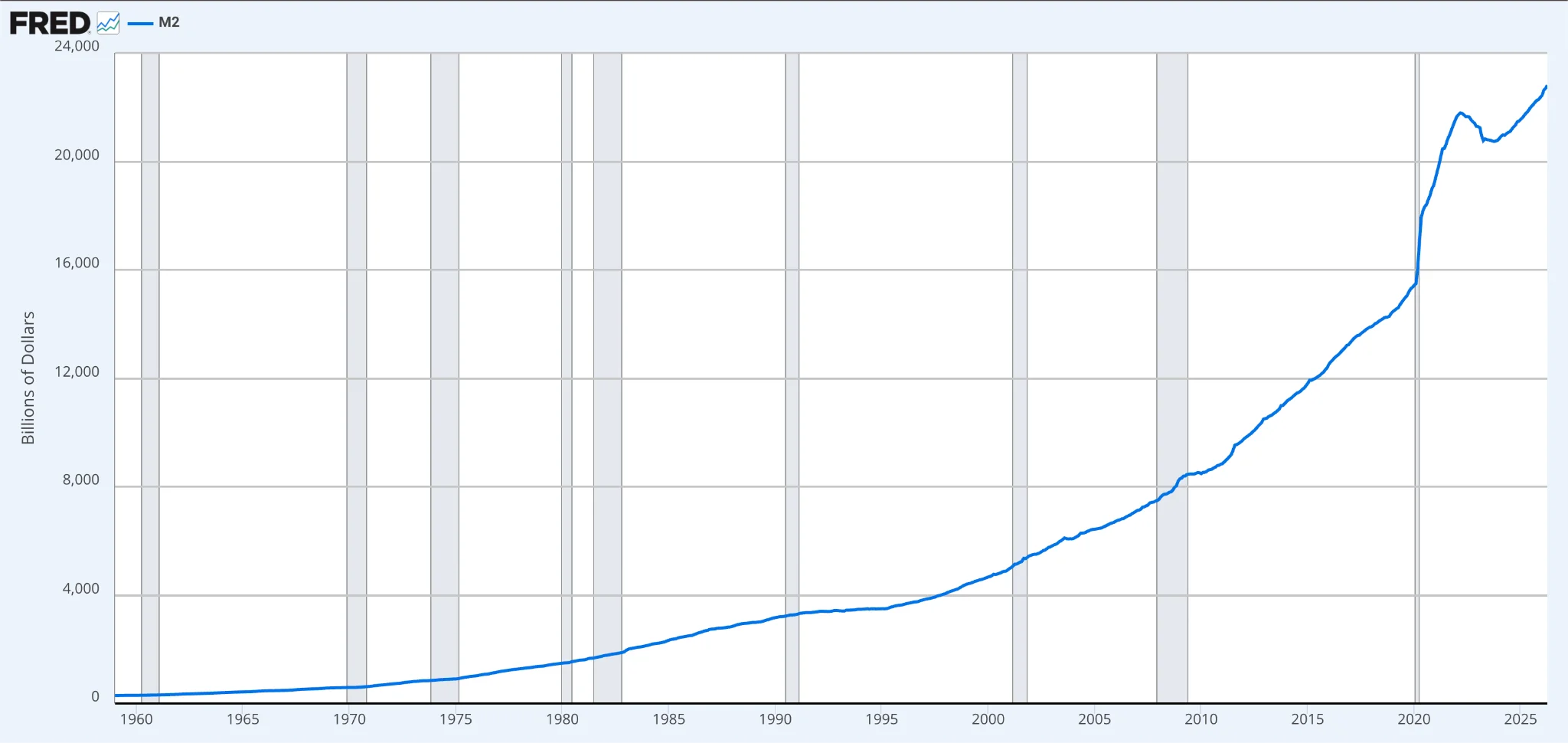

The fact that surprises most people: governments and central banks don’t create most of the money in circulation. Commercial banks do, and not by lending out savers’ deposits, but by issuing new loans. As the Bank of England explains in its 2014 paper “Money creation in the modern economy,” whenever a bank makes a loan it simultaneously creates a new deposit in the borrower’s account. This is new money, conjured by the act of lending. The total money stock expands and contracts largely through this private lending, a dynamic explored in global liquidity and the M2 money supply.

The mechanism is simpler than most people expect: a borrower applies for a loan, the bank approves it and books the loan as an asset. It simultaneously creates a matching deposit in the borrower’s account, which the borrower can now spend, and the money supply expands. The common misconception is that banks mainly lend out money savers have already deposited. They don’t: loans create deposits.

A system that can expand the money supply tends to let purchasing power leak away. By the US Bureau of Labor Statistics’ own Consumer Price Index, the dollar has lost roughly 96-97% of its purchasing power since the Federal Reserve was created in 1913. This basically means that a 1913 dollar buys only a few cents’ worth of goods today. Warren Buffett put it bluntly in 1977, calling inflation “a far more devastating tax” than any lawmakers could impose, precisely because it’s quiet and unlegislated.

When trust in the printing press fails entirely, things turn surreal. In 1923 Weimar Germany, prices doubled so fast that workers were paid twice a day and rushed to spend before their wages evaporated; banknotes grew so worthless that people reportedly burned them for warmth, the paper being cheaper than firewood. Zimbabwe later went one better, issuing a single hundred-trillion-dollar note. Scarcity, it turns out, is the whole point.

Central banks can also create money directly. In crises they’ve used quantitative easing, creating new reserves to buy government bonds and other assets, injecting money into the system to lower interest rates and support lending. Set by institutions like the Federal Reserve and its FOMC, these are the instruments of monetary policy.

Modern money: Benefits and Trade-offs

Modern monetary systems are powerful because they can expand credit, stabilize markets, and move value quickly, but each advantage comes with a corresponding risk.

FeatureBenefitRiskFiat currencyFlexible monetary policyInflation and debasementBank-created creditSupports lending and growthCredit bubbles and bustsQuantitative easingStabilizes markets in crisesAsset-price inflation and moral hazardDigital paymentsFast and convenientLess privacyCBDCsEfficient state-backed digital settlementPotential surveillance or controlCryptocurrenciesIndependent monetary networksVolatility, scams, and regulatory uncertaintyFeatureFiat currencyBenefitFlexible monetary policyRiskInflation and debasementFeatureBank-created creditBenefitSupports lending and growthRiskCredit bubbles and bustsFeatureQuantitative easingBenefitStabilizes markets in crisesRiskAsset-price inflation and moral hazardFeatureDigital paymentsBenefitFast and convenientRiskLess privacyFeatureCBDCsBenefitEfficient state-backed digital settlementRiskPotential surveillance or controlFeatureCryptocurrenciesBenefitIndependent monetary networksRiskVolatility, scams, and regulatory uncertainty

Underneath all of it sits one load-bearing assumption: trust. Fiat money works for exactly as long as people trust the institutions that issue and manage it. Keynes saw the danger in 1919, warning that there is no surer way to “overturn the existing basis of society” than to debauch the currency, to inflate it until faith collapses. So what happens to money when that trust erodes? That question is driving the next chapter.

The Future of Money: Digital, Decentralised, or Both?

For the first time in history, money’s form is being contested on multiple fronts at once. Underneath the specifics, it’s the same old tug-of-war between competing priorities: stability versus flexibility, privacy versus convenience, centralization versus decentralization, government control versus market choice, and speed versus resilience. The future of money is ultimately a debate about which trade-offs society prefers. Four developments are reshaping the answer.

FormOptimized forTrade-offCashPrivacy and resilienceLess convenient onlineBank depositsEase of useDependence on banksStablecoinsFast global settlementIssuer trustCBDCsState-backed digital moneyPrivacy concernsBitcoinScarcity and decentralizationVolatilityDeFi assetsOpen financial infrastructureComplexity and smart-contract riskFormCashOptimized forPrivacy and resilienceTrade-offLess convenient onlineFormBank depositsOptimized forEase of useTrade-offDependence on banksFormStablecoinsOptimized forFast global settlementTrade-offIssuer trustFormCBDCsOptimized forState-backed digital moneyTrade-offPrivacy concernsFormBitcoinOptimized forScarcity and decentralizationTrade-offVolatilityFormDeFi assetsOptimized forOpen financial infrastructureTrade-offComplexity and smart-contract risk

Cryptocurrencies

Cryptocurrencies are digitally-native money secured by cryptography and recorded on a blockchain, a shared digital ledger that no single party controls. They matter to the money question because they are the first serious attempt to build money that needs no government and no bank to function. The space has since expanded into thousands of altcoins and entire systems for lending and trading without intermediaries — decentralised finance, or DeFi.

Bitcoin as money

How does Bitcoin score against the six properties? Strong on scarcity (its supply is capped at 21 million), portability (it moves globally in minutes), and divisibility (each coin splits into 100 million units). Weaker on everyday acceptability, most shops still don’t take it, and on short-term store-of-value stability, since its price swings sharply.

That volatility cuts deep. On 22 May 2010, a programmer named Laszlo Hanyecz paid 10,000 bitcoin for two Papa John’s pizzas, coins then worth about $41. The same stash would later be worth hundreds of millions of dollars, making those very possibly the priciest pizzas in history and a permanent monument to Bitcoin’s price swings. Whether those swings are growing pains or a permanent flaw is the heart of debates over Bitcoin as a store of value and Bitcoin as an inflation hedge, and how it stacks up against the classic hard asset in Bitcoin vs gold.

Stablecoins

Stablecoins are the compromise layer in digital money: crypto tokens designed to keep a steady price, usually by tracking a fiat currency such as the US dollar. They are not trying to be hard money like Bitcoin. They are trying to make dollars move with crypto-like speed: across borders, around the clock, and on blockchain rails.

The biggest stablecoins, including USDT and USDC, are designed to trade at or near $1. That makes them useful for moving value between exchanges, sending digital dollars internationally, and avoiding crypto volatility without leaving the crypto ecosystem.

But the word “stable” can be misleading. A stablecoin is only as reliable as the mechanism behind it. Reserve-backed stablecoins depend on the quality of their assets, transparency, banking partners, and the issuer’s ability to honor redemptions. In March 2023, USDC briefly lost its $1 peg after part of its reserves were caught up in the Silicon Valley Bank collapse, showing that even regulated, reserve-backed stablecoins can carry real-world banking risk.

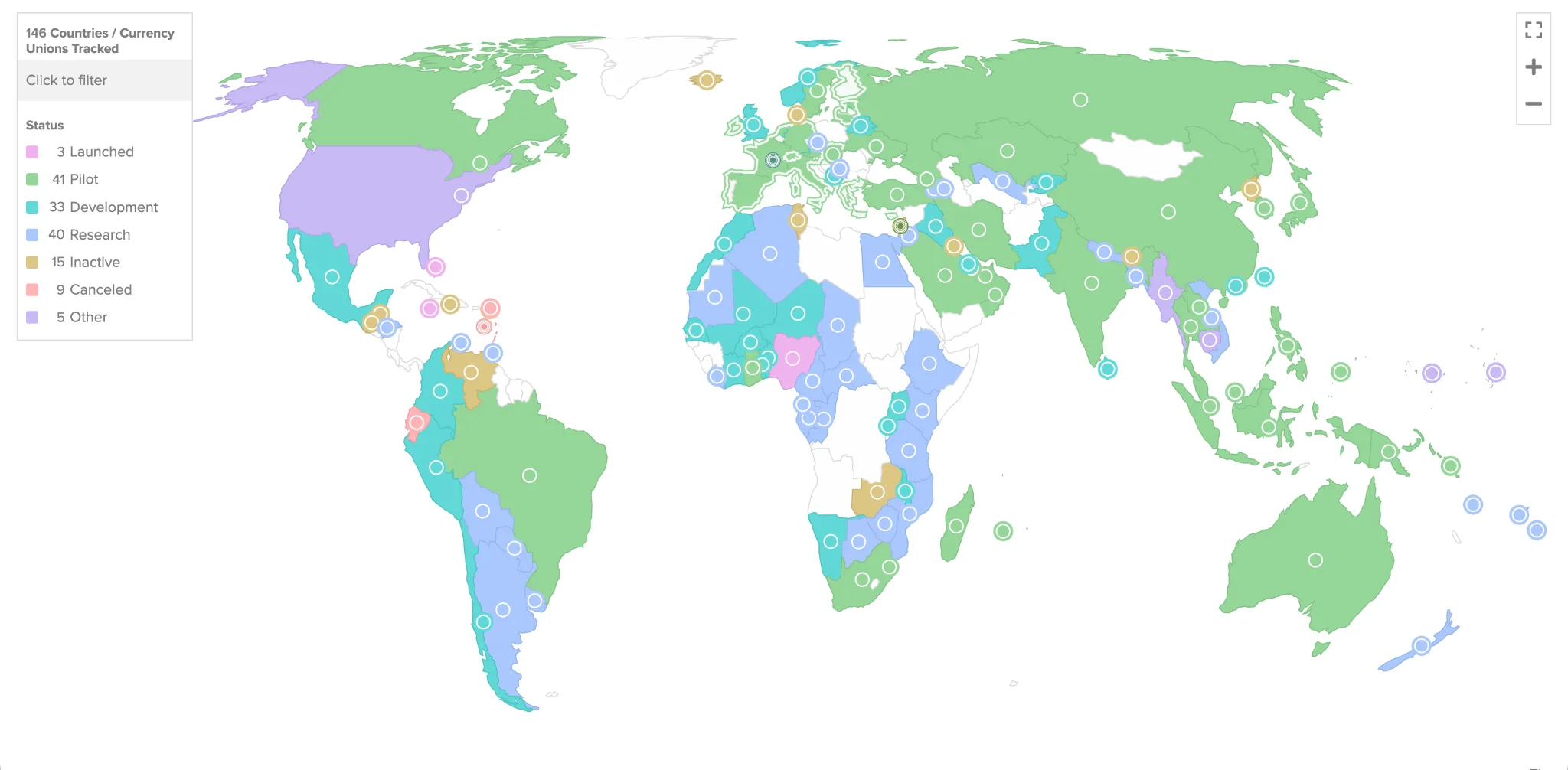

Central bank digital currencies, or CBDCs

A central bank digital currency is a government’s own answer to digital money, a digital version of national currency issued directly by the central bank. Governments are drawn to CBDCs for faster payments, lower cash-handling costs, and tighter control over monetary policy. The trade-off is privacy: unlike cash, a CBDC can in principle let the issuer see, and even restrict, how every unit is spent — which is why they remain controversial.

The cashless society

Beneath these specific technologies runs a broader trend: the steady disappearance of physical cash. Card payments, mobile wallets, and instant bank transfers already dominate everyday spending across much of the world, and several countries are nearly cashless. The convenience is real, but so is what’s lost when notes and coins vanish. Cash is:

- Private: leaves no transaction record.

- Resilient: works when networks go down or the power fails.

- Inclusive: serves the unbanked, the elderly, and anyone shut out of the digital financial system.

- Instant: a transaction settles the same second, with no intermediary.

A fully cashless society trades those quiet protections for efficiency, a bargain that deserves scrutiny rather than a shrug. For these reasons, many economists expect cash usage to keep shrinking without disappearing entirely.

Conclusion

Money has always evolved alongside the technology of its age: from cattle and shells to stamped metal, from paper claims to government fiat, and now to bits on a network. Each form was adopted because it served money’s functions better than what came before, and each was eventually challenged when something served them better still.

The core lesson: Money changes constantly, but the criteria for good money rarely do. Every monetary system (gold, dollars, stablecoins, or Bitcoin) is judged by the same question: how well does it store and transfer value across time and society?

The open question is not whether money will keep changing, but which form best satisfies the same six properties that have governed good money for three thousand years: durability, portability, divisibility, uniformity, scarcity, and acceptability. Whatever wins, these fundamentals are the lens that makes sense of every headline about inflation, digital dollars, and crypto.