Inflation is the rate at which the general level of prices for goods and services rises over time, reducing what each unit of money can buy. When inflation is positive, the same $100 buys a little less each year. It is normally expressed as an annual percentage, which economists call the inflation rate.

That single percentage shapes your grocery bill, your wages, the interest on your savings, the cost of borrowing, and the value of the money sitting in your bank account right now.

This guide explains, in plain English, what inflation means, how it is measured, what causes it, whether it is actually bad, who wins and loses from it, and the practical ways people try to protect their money. It also covers why Bitcoin keeps turning up in the inflation debate, and why the “hedge” label comes with serious caveats.

Key Takeaways

- Inflation means prices rise over time, so each unit of money buys less.

- The inflation rate is usually expressed as an annual percentage.

- CPI is the best-known inflation measure, but the Federal Reserve targets PCE inflation.

- Inflation can come from money supply growth, excess demand, supply shocks, wage-price spirals, and expectations.

- Mild, stable inflation can be healthy; high or unpredictable inflation damages savings, wages, planning, and trust.

- Inflation tends to benefit borrowers and asset owners while hurting cash savers, fixed-income households, and lenders.

- Protecting against inflation usually means holding assets that preserve purchasing power better than idle cash.

- Bitcoin is sometimes pitched as an inflation or debasement hedge because of its fixed supply, but its volatility means it has not behaved like a reliable short-term inflation hedge.

How Inflation Erodes Purchasing Power

The clearest way to understand inflation is through purchasing power, or how much a fixed amount of money can actually buy. The number of dollars in your wallet stays the same; what quietly shrinks is what each one is worth.

The classic example is a carton of milk. If milk costs $3 today and prices rise 3% a year, that same carton costs about $4 in roughly a decade. The dollar held still. The price moved, because each dollar now commands less milk.

(It is the same logic behind the old joke about paying more for the haircut you used to get for half the price, back when you still had the hair.)

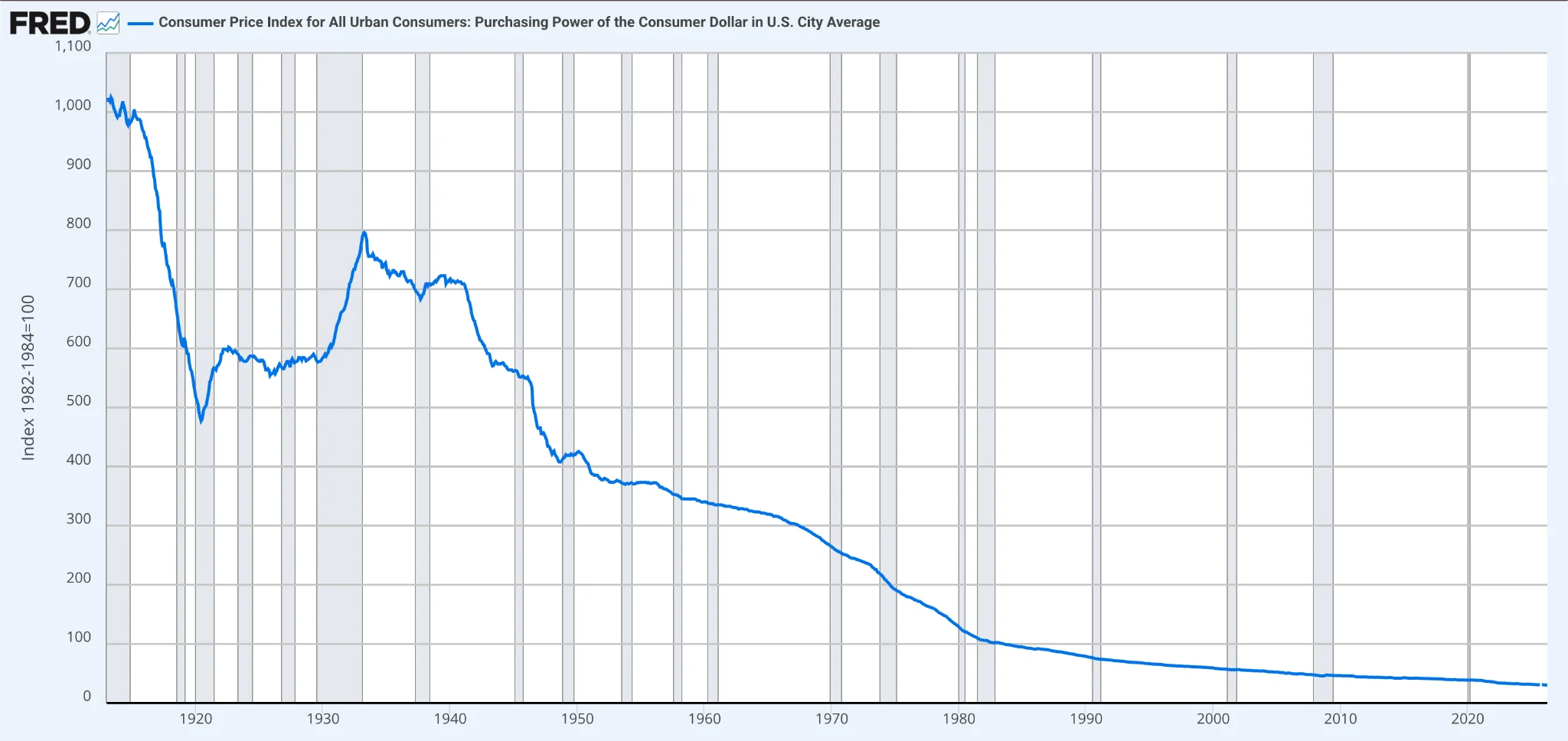

Zoom out and the effect compounds. Using the BLS CPI-U series, the U.S. dollar has lost roughly 97% of its purchasing power since 1913, meaning a 1913 dollar buys only a few cents’ worth of goods in today’s prices. The BLS inflation calculator uses the Consumer Price Index for All Urban Consumers, U.S. city average, for all items.

Over a more relatable span, what cost $100 in 2006 costs roughly $165 in 2026, depending on the month used for comparison. Put the other way, $100 today buys only about what $60 did around 2006.

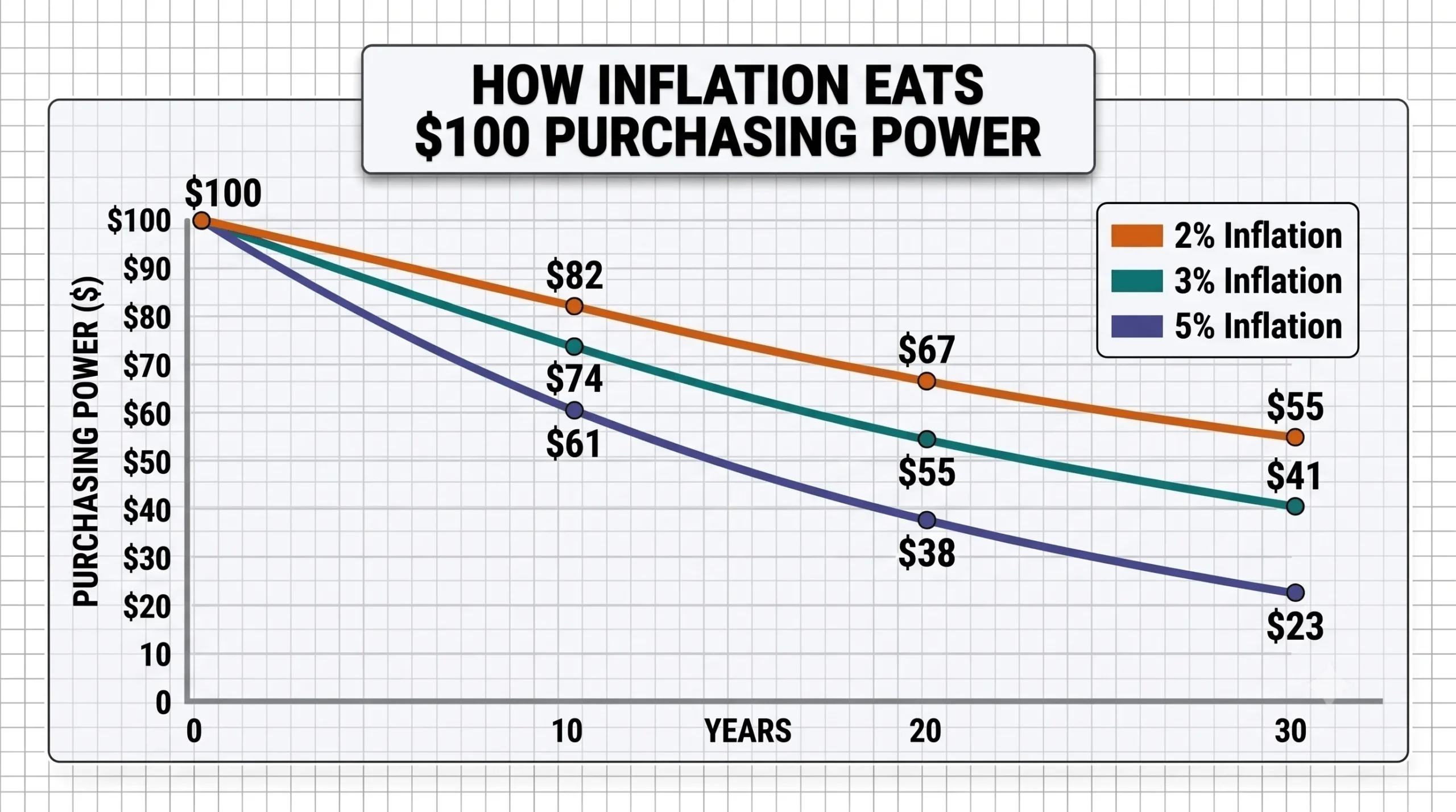

This is the reason every later section matters: money left idle loses value by default. A savings account paying 1% while inflation runs 3% shrinks in real terms. That’s because you hold more dollars, but less buying power. Even a “low” 3% rate roughly halves your money’s purchasing power over about 23 years.

How fast inflation cuts purchasing power

Inflation compounds over time, so even small annual price increases can meaningfully reduce what cash can buy.

Annual inflationYears to lose ~half of purchasing powerWhat it means2%~35 yearsSlow erosion3%~23 yearsNoticeable over a working life5%~14 yearsFast erosion8%~9 yearsSevere erosion10%~7 yearsVery damagingAnnual inflation2%Years to lose ~half of purchasing power~35 yearsWhat it meansSlow erosionAnnual inflation3%Years to lose ~half of purchasing power~23 yearsWhat it meansNoticeable over a working lifeAnnual inflation5%Years to lose ~half of purchasing power~14 yearsWhat it meansFast erosionAnnual inflation8%Years to lose ~half of purchasing power~9 yearsWhat it meansSevere erosionAnnual inflation10%Years to lose ~half of purchasing power~7 yearsWhat it meansVery damaging

The higher the rate, the faster cash loses real value. This is why even moderate inflation matters over long periods: the damage compounds quietly in the background.

How Is Inflation Measured?

You cannot manage what you cannot measure, so governments track inflation using price indexes: baskets of goods and services priced repeatedly over time. The International Monetary Fund defines inflation as the rate of increase in prices over a given period, usually measured broadly across the cost of living or the overall price level.

There is no single perfect inflation number. CPI, core CPI, PCE, PPI, and the GDP deflator each measure a different slice of the economy.

What is the inflation rate?

The inflation rate is the headline number you see in the news: the percentage change in a price index over a period, most often year-over-year, this month’s prices compared with the same month a year earlier. When a report says “inflation was 4.2%,” the chosen basket of goods cost 4.2% more than it did twelve months ago.

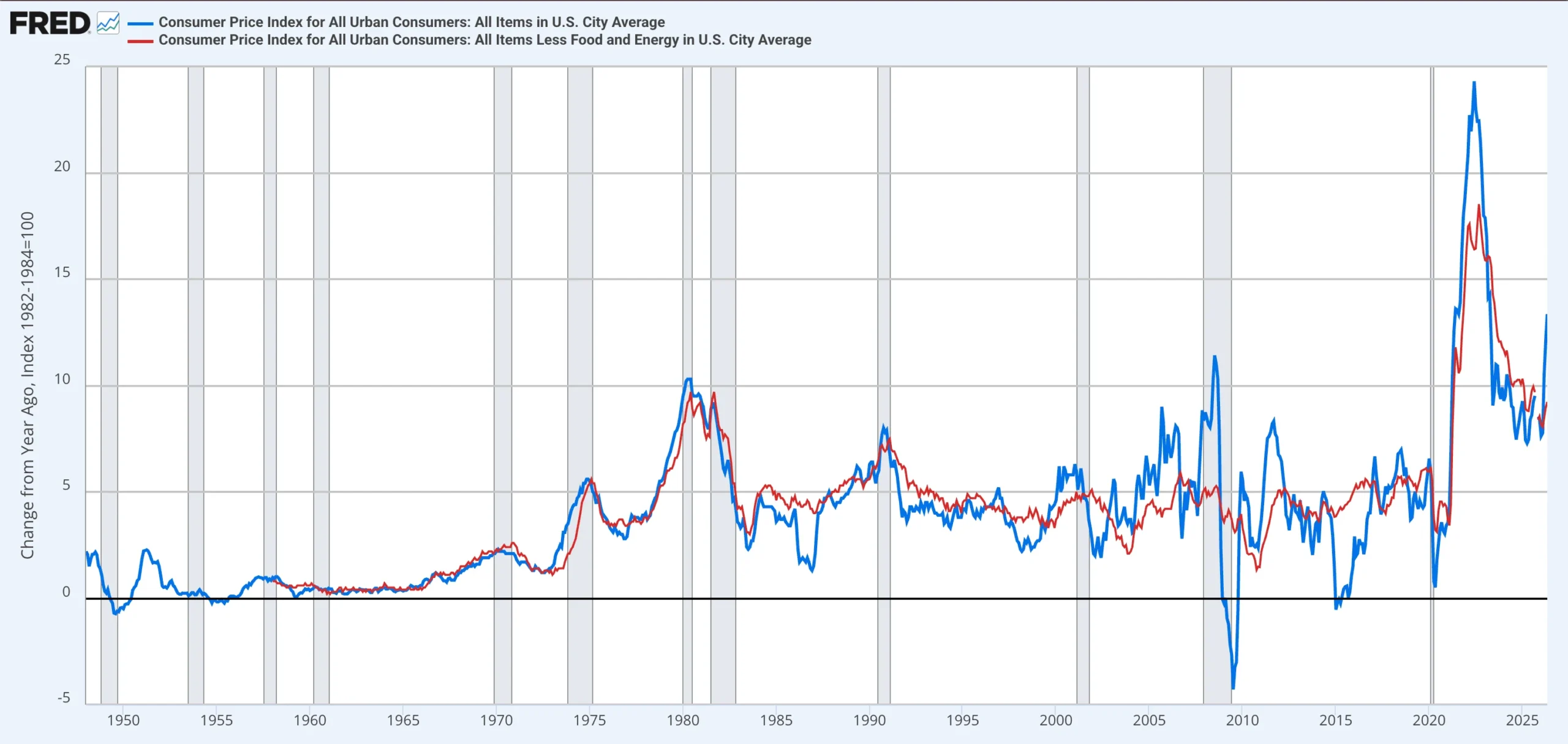

As of the May 2026 CPI report, the U.S. Consumer Price Index for All Urban Consumers rose 0.5% for the month and 4.2% over the previous 12 months, according to the Bureau of Labor Statistics. Core CPI, which excludes food and energy, rose 2.9% over the same period. Because this data changes every month, any exact figure should be date-stamped.

Consumer Price Index (CPI)

The Consumer Price Index is the best-known gauge. It tracks the average change over time in the prices urban consumers pay for a market basket of goods and services, and the BLS publishes it for the U.S. and for various geographic areas.

The basket spans food, housing, transportation, medical care, clothing, recreation, education, communication, and other everyday expenses, each weighted by how much consumers typically spend on it. Housing carries a large weight, which is why shelter costs can move the headline number so much. When most people say “inflation,” they usually mean CPI.

Headline vs. core inflation

Headline inflation includes everything in the basket. Core inflation strips out food and energy, the two most volatile categories. Food and energy prices swing on weather, harvests, oil prices, shipping snags, and geopolitics. A sudden gasoline spike can lift headline inflation even when the underlying trend is calmer.

Economists and central banks watch core inflation because it gives a cleaner read on that trend, which does not mean food and energy stop mattering. Households still buy groceries and fuel. Core inflation simply helps separate temporary shocks from more persistent pressure.

Producer Price Index (PPI)

The Producer Price Index measures prices from the seller’s side, or what producers receive for their output before it reaches consumers. The BLS describes it as a family of indexes tracking the average change over time in selling prices received by domestic producers. Because cost increases at the factory, farm, or wholesale level often pass through to shoppers later, PPI can act as an early warning that consumer inflation may follow.

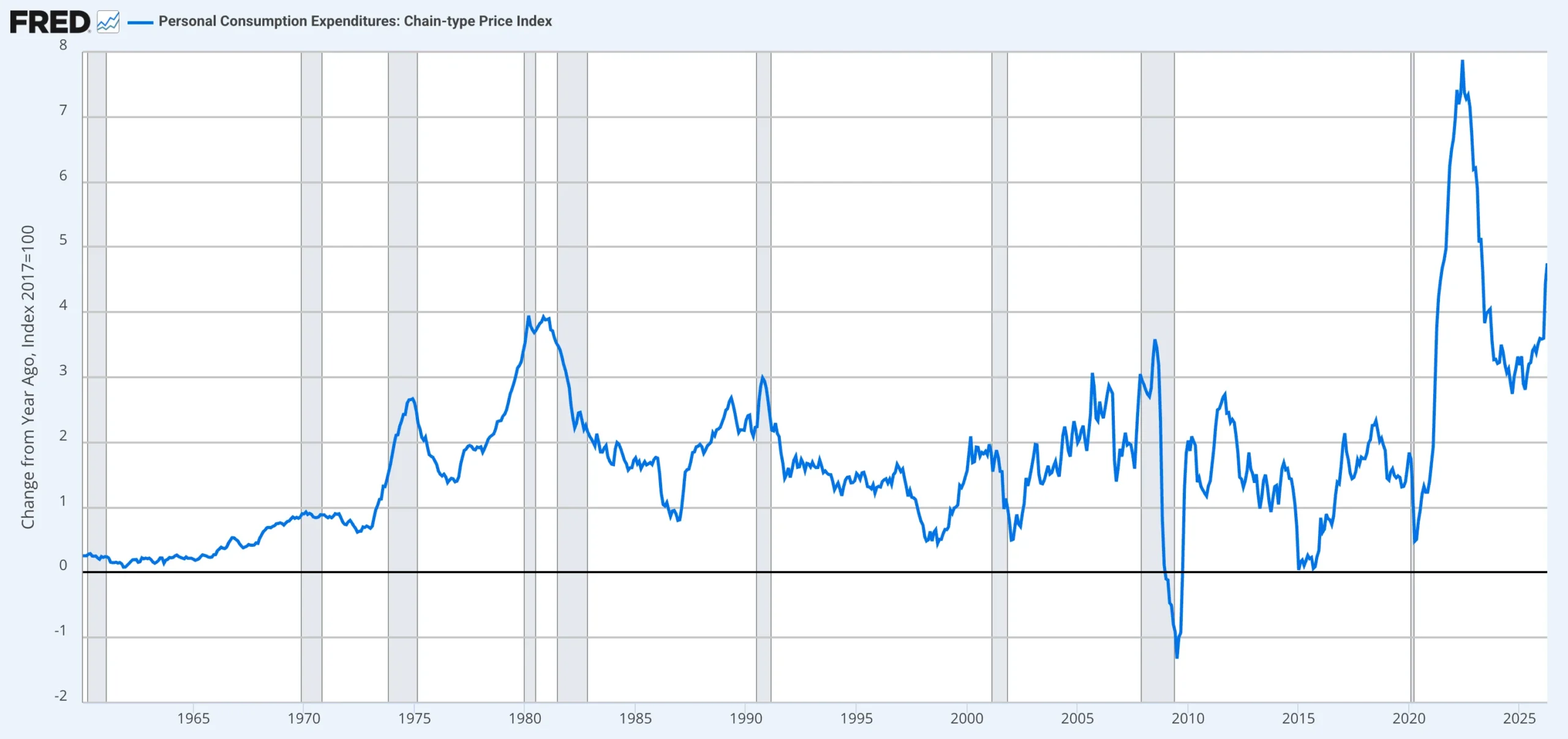

PCE: the Fed’s preferred gauge

Here is a detail most explainers skip: the Federal Reserve does not target CPI. It targets the Personal Consumption Expenditures price index, or PCE.

The BEA says the PCE price index reflects changes in the prices of goods and services purchased by consumers in the United States. As of the April 2026 reading, PCE prices were up 3.8% from a year earlier.

The Fed prefers PCE because it covers a broader range of spending and adjusts faster when consumers change behavior. If beef gets expensive and people switch to chicken, PCE captures that substitution more readily than CPI. When the Fed talks about its 2% target, it means 2% PCE inflation over the longer run.

GDP deflator

The broadest measure is the GDP deflator, which captures price changes across the whole economy rather than a single consumer basket. The BEA says it measures changes in the prices of goods and services produced in the United States, including exports while excluding imports. That makes it useful for economy-wide inflation, though it is less timely and less familiar to households than CPI.

How to calculate the inflation rate

The formula is straightforward:

Inflation rate = ((Current index − Previous index) ÷ Previous index) × 100

Worked example: suppose a price index reads 300.0 today and read 291.0 a year ago.

(300.0 − 291.0) ÷ 291.0 × 100 = 3.1%

That is the annual inflation rate, and the same arithmetic works on official CPI, PCE, PPI, or GDP deflator data. The formula also makes an important point clear: inflation measures the rate at which prices change, not how high they are. If inflation slows from 8% to 3%, prices are still rising, just more slowly.

Main inflation measures compared

Inflation is measured in several ways because different indicators track different parts of the economy, from household prices to producer costs to economy-wide price changes.

MeasureWhat it coversPublisherKey useMain limitationCPIConsumer basketBLSHeadline consumer inflationFixed-basket issues, shelter lagCore CPICPI excluding food and energyBLSUnderlying inflation trendExcludes things households still buyPCEBroader consumer spendingBEAThe Fed’s 2% targetLess familiar to the publicPPIPrices producers receiveBLSEarly-warning signalNot a direct consumer-price measureGDP deflatorWhole economyBEABroadest economy-wide measureLess timely than CPIMeasureCPIWhat it coversConsumer basketPublisherBLSKey useHeadline consumer inflationMain limitationFixed-basket issues, shelter lagMeasureCore CPIWhat it coversCPI excluding food and energyPublisherBLSKey useUnderlying inflation trendMain limitationExcludes things households still buyMeasurePCEWhat it coversBroader consumer spendingPublisherBEAKey useThe Fed’s 2% targetMain limitationLess familiar to the publicMeasurePPIWhat it coversPrices producers receivePublisherBLSKey useEarly-warning signalMain limitationNot a direct consumer-price measureMeasureGDP deflatorWhat it coversWhole economyPublisherBEAKey useBroadest economy-wide measureMain limitationLess timely than CPI

The challenges of measuring inflation

Measuring inflation sounds simple but is genuinely hard: no agency can track every price for every product everywhere. Statisticians sample a basket and update it periodically, which forces unavoidable judgment calls.

The thorniest issue is quality change. A smartphone costs more than a basic mobile phone did in 2007, but it is also vastly more capable. So, a part of that higher price buys a better product, not inflation. Statisticians make quality adjustments to separate the two, and reasonable people disagree about how.

Substitution is another challenge: when beef gets expensive and shoppers switch to chicken, a fixed basket can overstate the pain they actually feel. A subtler version is shrinkflation: the shelf price stays the same while the package shrinks. A cereal box drops from 18 ounces to 16 at the same price, a hidden increase per ounce that the sticker never shows.

So your personal experience of inflation can differ from the official number. A household that spends heavily on rent, fuel, childcare, or groceries may feel a sharper squeeze than the national average suggests.

Measurement challengeWhy it mattersQuality changesA higher price may partly reflect a better productSubstitutionPeople change what they buy when prices riseShrinkflationPackage sizes can fall while shelf prices holdRegional differencesHousing, food, and fuel prices vary by locationPersonal spending mixYour inflation rate depends on what you buyShelter lagHousing data can move slowly versus real-time rentsDiscounts and promotionsTemporary price cuts can muddy the trendMeasurement challengeQuality changesWhy it mattersA higher price may partly reflect a better productMeasurement challengeSubstitutionWhy it mattersPeople change what they buy when prices riseMeasurement challengeShrinkflationWhy it mattersPackage sizes can fall while shelf prices holdMeasurement challengeRegional differencesWhy it mattersHousing, food, and fuel prices vary by locationMeasurement challengePersonal spending mixWhy it mattersYour inflation rate depends on what you buyMeasurement challengeShelter lagWhy it mattersHousing data can move slowly versus real-time rentsMeasurement challengeDiscounts and promotionsWhy it mattersTemporary price cuts can muddy the trend

What Causes Inflation?

Inflation has several drivers, and real-world episodes usually mix more than one. In short, inflation tends to appear when money, demand, costs, wages, or expectations rise faster than the economy’s ability to produce goods and services. Economists group the causes into a few classic mechanisms.

CauseSimple explanationExampleMoney supply growthMoney grows faster than goods and servicesDeficit monetization, rapid credit expansionDemand-pullBuyers want more than the economy can produceStimulus-fueled spending boomCost-pushInput costs rise and businesses pass them onOil, food, shipping, energy shocksWage-price spiralWages and prices push each other higherWorkers win raises, firms raise pricesExpectationsPeople expect inflation and act accordinglyFirms pre-emptively raise pricesCauseMoney supply growthSimple explanationMoney grows faster than goods and servicesExampleDeficit monetization, rapid credit expansionCauseDemand-pullSimple explanationBuyers want more than the economy can produceExampleStimulus-fueled spending boomCauseCost-pushSimple explanationInput costs rise and businesses pass them onExampleOil, food, shipping, energy shocksCauseWage-price spiralSimple explanationWages and prices push each other higherExampleWorkers win raises, firms raise pricesCauseExpectationsSimple explanationPeople expect inflation and act accordinglyExampleFirms pre-emptively raise prices

Money supply: the monetarist view

The monetarist explanation is the most fundamental: when the money supply grows faster than the supply of goods and services, more money chases the same output, and prices rise. As Milton Friedman argued, inflation is “always and everywhere a monetary phenomenon” in the sense that it comes from money growing faster than output.

That does not make every episode simple. Quantitative easing, commercial-bank lending, government deficits, and private credit cycles affect money and liquidity in different ways, and their inflationary punch depends on whether that money translates into real spending. Still, the core idea is intuitive: if money expands much faster than the goods available to buy, each unit tends to lose value.

Bitcoin enters the debate here because it was designed with a very different monetary policy. Dollars, euros, and pounds can expand through central-bank policy, bank lending, and government borrowing. Bitcoin’s issuance follows a predetermined schedule, and its consensus code caps the supply at 21 million BTC. That is why supporters frame it as a hedge against long-term currency debasement: if fiat can be expanded and Bitcoin cannot, the argument goes, Bitcoin may hold purchasing power better over very long periods.

Demand-pull inflation

Demand-pull inflation is the “too much money chasing too few goods” story. When demand outstrips what the economy can produce (from booming consumer spending, stimulus, easy credit, or rapid wage gains) sellers can raise prices because buyers will pay. It is the inflation of a hot economy. The surge after pandemic lockdowns lifted is a clean example: households had savings and stimulus, demand rebounded fast, and supply chains were still constrained.

Cost-push inflation (supply shocks)

Cost-push inflation comes from the supply side: when a key input jumps in price, producers pass it on. The textbook case is oil. A spike in crude raises the cost of manufacturing, shipping, heating, flying, farming, and commuting, pushing prices up across the economy even if demand has not changed. Wars, droughts, blocked shipping routes, and broken supply chains all do the same. The energy and commodity shock after Russia’s 2022 invasion of Ukraine rippled from fuel into food, fertilizer, and transportation.

Built-in inflation and the wage-price spiral

Built-in inflation is self-perpetuating. As prices rise, workers demand higher wages to keep up; higher wages raise business costs, so firms raise prices again, which prompts another round of wage demands. This is the wage-price spiral, and it is dangerous because inflation can keep running long after the original trigger fades. Once contracts, wage negotiations, business pricing, and household expectations all adjust to higher inflation, the pattern becomes hard to reverse. See our guide to [LINK: Wage-Price Spiral].

Inflation expectations

Expectations can be self-fulfilling. If businesses expect costs to rise, they raise prices early. If workers expect prices to rise, they bargain for larger increases. If consumers expect prices to rise quickly, they buy sooner, adding demand today. That behavior makes inflation stickier — which is why central banks work so hard to keep expectations “anchored.” When people trust that inflation will return to target, temporary shocks tend to stay temporary. When that trust breaks, inflation gets much harder to control.

Types of Inflation

Inflation is often classified by how fast prices rise, a ladder of severity.

TypeRoughly how fastCharacterCreepingLow single digits a yearMild, predictable, generally healthyWalkingMid-to-high single digitsNoticeable; starts to worry policymakersGallopingDouble or triple digits a yearDestabilizing; savings erode quicklyHyperinflationOften over 50% per monthMoney collapses as a store of valueTypeCreepingRoughly how fastLow single digits a yearCharacterMild, predictable, generally healthyTypeWalkingRoughly how fastMid-to-high single digitsCharacterNoticeable; starts to worry policymakersTypeGallopingRoughly how fastDouble or triple digits a yearCharacterDestabilizing; savings erode quicklyTypeHyperinflationRoughly how fastOften over 50% per monthCharacterMoney collapses as a store of value

The catastrophic top of the ladder is hyperinflation. The most cited case is Weimar Germany in 1923, when the government printed million- and billion-mark notes and, per Britannica, one U.S. dollar came to equal about a trillion marks by November. The everyday absurdity is what sticks: Britannica recounts a German student who ordered a cup of coffee priced at 5,000 marks, only to be charged 7,000 for a second cup by the time he finished the first. When money loses credibility, people rush to spend it before it loses even more value.

Two more named conditions are worth knowing, and are frequently searched:

- Stagflation: the rare, painful combination of high inflation and a stagnant economy with high unemployment. It broke older economic models when it struck in the 1970s and remains one of the scenarios policymakers fear most.

- Disinflation: a slowdown in the inflation rate while prices are still rising. Inflation easing from 6% to 3% is disinflation. Falling prices are a separate phenomenon called deflation.

TermWhat prices are doingSimple exampleInflationRisingInflation goes from 3% to 5%DisinflationRising, but more slowlyInflation falls from 6% to 3%DeflationFallingInflation turns negative, at −1%StagflationRising, while growth is weakHigh inflation plus high unemploymentTermInflationWhat prices are doingRisingSimple exampleInflation goes from 3% to 5%TermDisinflationWhat prices are doingRising, but more slowlySimple exampleInflation falls from 6% to 3%TermDeflationWhat prices are doingFallingSimple exampleInflation turns negative, at −1%TermStagflationWhat prices are doingRising, while growth is weakSimple exampleHigh inflation plus high unemployment

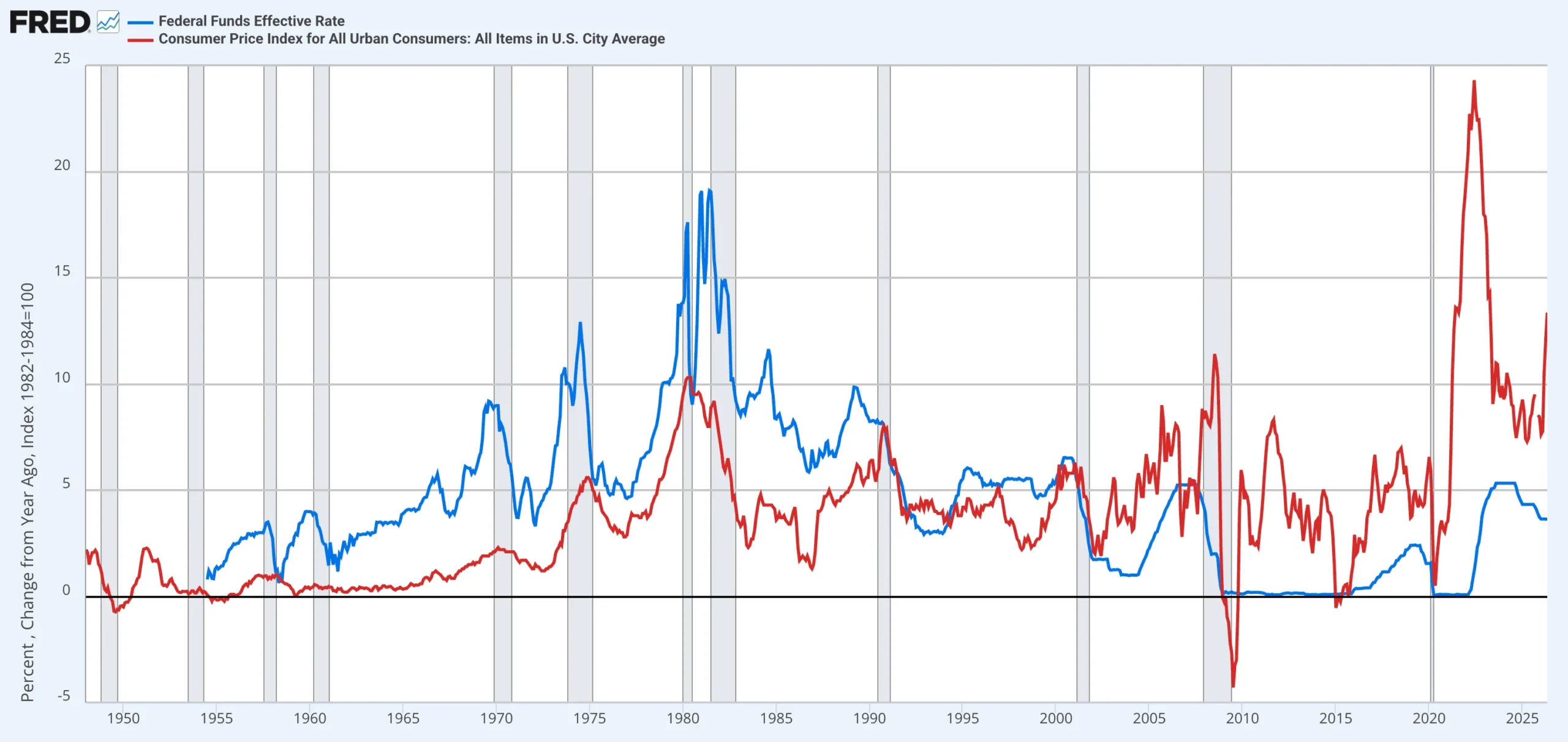

Central Banks, Interest Rates, and the 2% Target

This is the lever that connects inflation to every headline about the Federal Reserve. Modern central banks treat managing inflation as a core job, and they do it largely through interest rates and financial conditions.

Most major central banks aim for low, stable inflation rather than zero. In the United States, the Federal Reserve seeks 2% inflation over the longer run, measured by PCE, a goal it reaffirmed in its 2025 framework review. Why 2% and not zero? A small, steady amount of inflation gives the central bank room to cut rates in a downturn, reduces the risk of deflation, and lets wages and prices adjust more smoothly.

The main tool is the policy interest rate. When inflation runs hot, the central bank can raise rates, making borrowing more expensive and saving more attractive; that cools spending, investment, housing demand, hiring, and asset prices, easing upward pressure. When the economy is weak and inflation is too low, it can cut rates to make borrowing cheaper and stimulate demand.

Central bank actionIntended effectTrade-offRaise interest ratesCool demand, reduce inflation pressureSlower growth, weaker assets, higher debt costsLower interest ratesStimulate borrowing and spendingCan reignite inflationQuantitative easingSupport liquidity and financial conditionsCan lift asset prices and money growthQuantitative tighteningDrain liquidity from the systemCan tighten conditions sharplyForward guidanceShape expectationsLoses power if credibility weakensCentral bank actionRaise interest ratesIntended effectCool demand, reduce inflation pressureTrade-offSlower growth, weaker assets, higher debt costsCentral bank actionLower interest ratesIntended effectStimulate borrowing and spendingTrade-offCan reignite inflationCentral bank actionQuantitative easingIntended effectSupport liquidity and financial conditionsTrade-offCan lift asset prices and money growthCentral bank actionQuantitative tighteningIntended effectDrain liquidity from the systemTrade-offCan tighten conditions sharplyCentral bank actionForward guidanceIntended effectShape expectationsTrade-offLoses power if credibility weakens

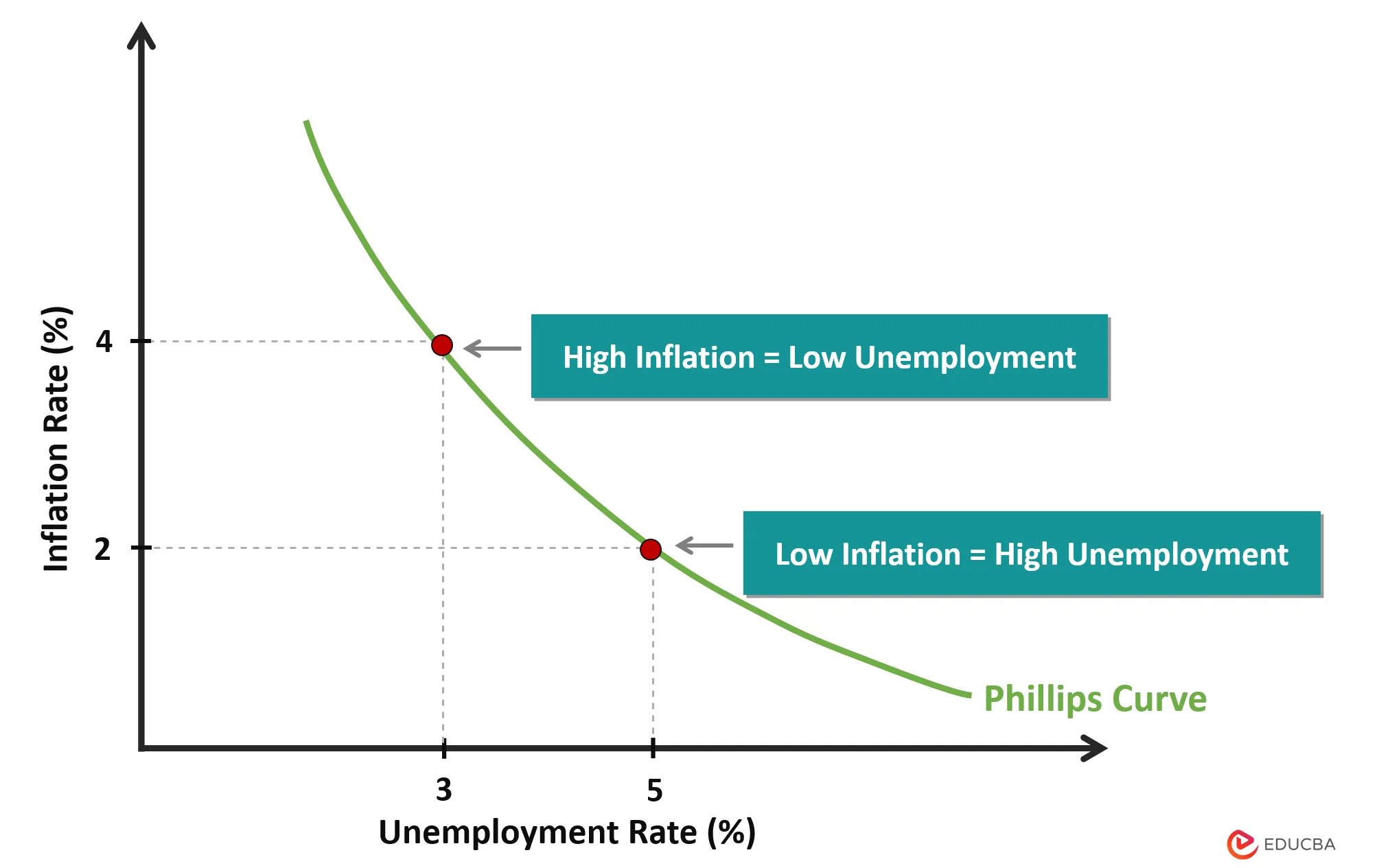

The catch is the growth trade-off: cooling inflation usually means slowing the economy. That tension is captured by the Phillips curve, the historically observed relationship between inflation and unemployment. The link is not reliable in every era, stagflation famously challenged it, but the underlying dilemma remains. This is why rate decisions dominate financial headlines. Each one is a bet on balance: move too slowly and inflation can entrench; move too aggressively and the economy can tip into recession.

Is Inflation Good or Bad?

The honest answer depends entirely on how much and how fast. Inflation’s effects range from helpful to catastrophic.

Inflation conditionHelpful or harmful?WhyLow and stableHelpfulSupports spending, reduces deflation riskModerate but risingConcerningStarts to bite into wages, savings, planningHigh and volatileHarmfulErodes trust and scrambles contractsHyperinflationCatastrophicMoney stops working as a store of valueDeflationDangerousCan trigger delayed spending and falling demandInflation conditionLow and stableHelpful or harmful?HelpfulWhySupports spending, reduces deflation riskInflation conditionModerate but risingHelpful or harmful?ConcerningWhyStarts to bite into wages, savings, planningInflation conditionHigh and volatileHelpful or harmful?HarmfulWhyErodes trust and scrambles contractsInflation conditionHyperinflationHelpful or harmful?CatastrophicWhyMoney stops working as a store of valueInflation conditionDeflationHelpful or harmful?DangerousWhyCan trigger delayed spending and falling demand

The case for mild inflation

A low, stable rate is widely considered healthy. It nudges people to spend and invest rather than hoard cash that is slowly losing value, supports gradual wage and asset growth, and keeps the economy a safe distance from deflation. That is why central banks aim for a positive 2% rather than 0%. Mild inflation can also help debtors: as incomes rise over time, a fixed-rate mortgage gets easier to repay in future dollars.

The dangers of high inflation

Ronald Reagan once called inflation “as violent as a mugger, as frightening as an armed robber” — campaign-trail hyperbole in 1978, but it captured how the era felt. When inflation climbs and turns unpredictable, the damage mounts: it erodes savings, scrambles business planning, punishes anyone on a fixed income, and discourages long-term lending, since no one wants to be repaid in money of unknown future value.

It also changes behavior. People spend faster, businesses reprice more often, workers bargain harder, and lenders demand higher interest rates. At the extreme of hyperinflation, money stops functioning as a store of value, and people flee into hard goods, foreign currency, gold, or barter because they no longer trust the currency.

The risk of deflation (the deflationary spiral)

The opposite of inflation carries its own danger. Deflation is a sustained fall in prices, which sounds appealing, goods get cheaper, but can turn toxic. If people expect prices to keep falling, they delay purchases. That cuts demand, so businesses cut production, wages, and jobs. Lower incomes cut demand further. This self-reinforcing loop is the deflationary spiral.

Who Wins and Who Loses From Inflation

Inflation quietly transfers wealth between groups. Writing in 1919, John Maynard Keynes warned that through “a continuing process of inflation,” governments can confiscate their citizens’ wealth “secretly and unobserved.”

(He famously credited the line to Lenin, though historians have never found it in Lenin’s own writings.) The mechanics are less sinister than that but just as real: inflation rewards some people and penalizes others, mostly depending on which side of a debt they sit.

WinnersWhy they can benefitBorrowers with fixed-rate debtThey repay loans with cheaper future dollarsGovernmentsInflation erodes the real value of public debtOwners of real assetsProperty, stocks, and businesses may rise with pricesBusinesses with pricing powerThey can raise prices to protect marginsWinnersBorrowers with fixed-rate debtWhy they can benefitThey repay loans with cheaper future dollarsWinnersGovernmentsWhy they can benefitInflation erodes the real value of public debtWinnersOwners of real assetsWhy they can benefitProperty, stocks, and businesses may rise with pricesWinnersBusinesses with pricing powerWhy they can benefitThey can raise prices to protect marginsLosersWhy they can be hurtSavers holding cashIdle money loses real purchasing powerLenders at fixed ratesThey are repaid in weaker dollarsPeople on fixed incomesPensions or annuities may not keep upWorkers whose wages lagPaychecks buy lessRenters with flexible costsEssentials can rise faster than incomeLosersSavers holding cashWhy they can be hurtIdle money loses real purchasing powerLosersLenders at fixed ratesWhy they can be hurtThey are repaid in weaker dollarsLosersPeople on fixed incomesWhy they can be hurtPensions or annuities may not keep upLosersWorkers whose wages lagWhy they can be hurtPaychecks buy lessLosersRenters with flexible costsWhy they can be hurtEssentials can rise faster than income

The pattern is consistent: inflation favors debtors and holders of real assets while penalizing savers, lenders, and anyone whose income is fixed in nominal terms.

How to Protect Your Money From Inflation

Because cash loses value by default, protecting your money means holding things that tend to keep pace with, or outrun, rising prices. The unifying idea is a store of value: an asset whose supply cannot be easily inflated may hold purchasing power better over time. No single hedge is perfect, and most people spread across several.

HedgeWhy people use itMain riskReal estateRents and values may rise with inflationIlliquid and rate-sensitiveGoldScarce asset with a long store-of-value historyNo income; can underperform for yearsStocksCompanies can raise prices over timeShort-term valuation pressureTIPSPrincipal adjusts with CPISensitive to real interest ratesI bondsInterest rate adjusts with inflationPurchase and redemption limitsBitcoinFixed-supply debasement-hedge thesisVery volatile; weak short-term CPI hedgeCashLiquidity and safetyLoses value when inflation tops interestHedgeReal estateWhy people use itRents and values may rise with inflationMain riskIlliquid and rate-sensitiveHedgeGoldWhy people use itScarce asset with a long store-of-value historyMain riskNo income; can underperform for yearsHedgeStocksWhy people use itCompanies can raise prices over timeMain riskShort-term valuation pressureHedgeTIPSWhy people use itPrincipal adjusts with CPIMain riskSensitive to real interest ratesHedgeI bondsWhy people use itInterest rate adjusts with inflationMain riskPurchase and redemption limitsHedgeBitcoinWhy people use itFixed-supply debasement-hedge thesisMain riskVery volatile; weak short-term CPI hedgeHedgeCashWhy people use itLiquidity and safetyMain riskLoses value when inflation tops interest

Real estate

Property is a traditional hedge: home values and rents often rise with the broader price level, and a fixed-rate mortgage is repaid in cheaper future dollars. The downsides are real: properties are illiquid, expensive to buy/sell, tied to local markets, and rate-sensitive. When central banks raise rates to fight inflation, mortgage costs climb and property values can come under pressure.

Gold

Gold has served as a store of value for thousands of years, and its slow supply growth underpins its reputation as an inflation hedge. The caveat is a mixed record over shorter horizons: it can stagnate or fall for years, and it produces no income, so its return depends entirely on price appreciation. Gold tends to matter most when investors lose confidence in paper money, central banks, or markets.

Stocks and equities

Equities are one of the most common real-world hedges. Companies can often raise prices alongside costs, so revenues and earnings may climb over time, and businesses with strong pricing power tend to weather inflation best. But stocks are no perfect hedge: high or rising inflation often pressures valuations in the short term as interest rates rise and investors demand higher returns.

Warren Buffett put the corporate cost vividly in his 1981 letter to Berkshire Hathaway shareholders, describing inflation as a “gigantic corporate tapeworm” that consumes a company’s capital regardless of how healthy the business is. Equities protect better over years than over weeks or months.

TIPS and I bonds

TIPS and I bonds are the textbook government-backed hedges. Treasury Inflation-Protected Securities (TIPS) adjust their principal up or down with inflation over their term; if the adjusted principal is higher than the original when the TIPS matures, the investor receives the larger amount. Series I savings bonds carry an inflation-linked component too.

For I bonds issued from May 1, 2026 through October 31, 2026, TreasuryDirect listed a composite rate of 4.26%, part of which resets with inflation every six months. Both are designed to preserve purchasing power, with trade-offs: purchase limits, redemption rules, tax considerations, and sensitivity to real interest rates.

Bitcoin and crypto

Bitcoin is the cryptoasset most often discussed as an inflation hedge. The argument is simple: unlike fiat currencies, whose supply can grow through central-bank policy, credit creation, and government borrowing, Bitcoin has a predictable issuance schedule and a hard 21-million cap. Supporters read that fixed supply as digital scarcity, which is why Bitcoin is so often compared with gold.

That makes Bitcoin relevant to inflation without making it a dependable hedge against it. Consumer inflation is measured by CPI or PCE, while Bitcoin’s price answers to many other forces: liquidity, interest rates, risk appetite, regulation, exchange flows, leverage, and crypto-specific events. A scarce asset can still fall hard when investors are dumping risk.

A useful framing: Bitcoin may work better as a hedge against long-term currency debasement than against short-term inflation readings. S&P Global drew a similar distinction in a 2026 report, arguing that Bitcoin functions more as a debasement hedge than an inflation hedge, while noting that its volatility remains higher than that of more traditional assets.

Access matters too. Some investors buy Bitcoin directly through an exchange or hold it in a wallet; others use regulated exchange-traded products. In January 2024, the SEC approved the listing and trading of several spot Bitcoin exchange-traded products, while stressing that approval was not an endorsement of Bitcoin itself.

Stablecoins are a different animal. A U.S. dollar stablecoin is not a hedge against U.S. dollar inflation, because it is built to track the dollar. If the dollar loses purchasing power, so does the stablecoin. But in countries facing much higher local-currency inflation or devaluation, dollar stablecoins offer a way to hold dollar exposure digitally. Chainalysis reported that Argentina’s long battle with inflation and peso devaluation pushed users toward USD-pegged stablecoins, with retail-sized stablecoin value received there growing faster than any other cryptoasset type in its data.

The balanced takeaway: Bitcoin and some crypto tools belong in the inflation conversation, especially around scarce assets, fiat debasement, and stores of value. But they carry major trade-offs: volatility, custody and exchange risk, regulatory uncertainty, and a far shorter history than gold, real estate, stocks, or government inflation-linked bonds.

Conclusion

Inflation is a permanent feature of modern economies, not a passing emergency. Prices drift upward, and money left idle loses value year after year. The aim is to understand it rather than fear it: how fast prices are rising, why, how policymakers respond, and which assets tend to preserve purchasing power better than cash.

A store of value, in whatever form fits your risk tolerance and time horizon, sits at the core of any defense. Real estate, gold, stocks, TIPS, I bonds, and Bitcoin all belong in that conversation, and none is perfect. Bitcoin’s fixed supply makes it relevant to the debate over fiat debasement; its volatility makes it risky as a short-term inflation hedge. Holding both of those facts at once is what separates a slogan from a real inflation strategy.