What Is Blockchain Technology?

Blockchain technology is a decentralized distributed ledger system capable of securely recording and storing digital asset data in blocks, which are linked through cryptographic hashes and arranged sequentially in a chain. This structure ensures transparency, immutability, and resistance to unauthorized changes or fraud.

History of Blockchain Technology

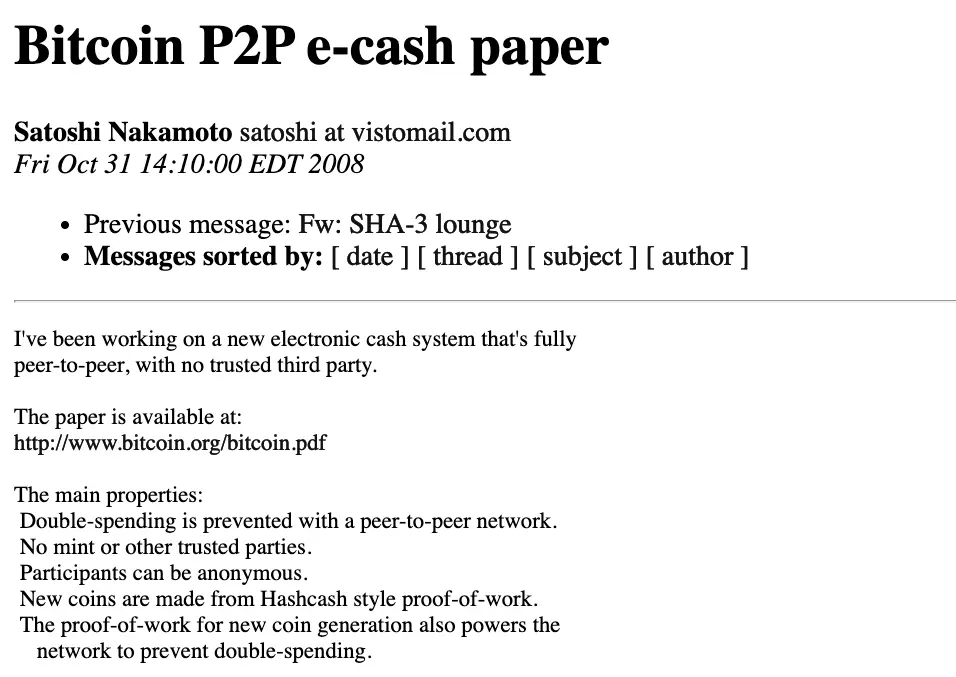

The concept of blockchain was introduced in the early 1990s by researchers Stuart Haber and W. Scott Stornetta. However, it gained global recognition in 2008 when the anonymous figure Satoshi Nakamoto released the white paper on Bitcoin, which established blockchain as the core technology powering the first cryptocurrency.

On January 3, 2009, the Bitcoin blockchain was officially launched with the mining of the first block (Genesis Block), which rewarded 50 BTC. The first Bitcoin transaction took place on January 12, 2009, when Satoshi Nakamoto sent 10 BTC to developer Hal Finney.

Blockchain Structure

A blockchain consists of interconnected blocks containing transaction data. Each block includes:

- Block Header: Contains critical metadata, such as the hash of the previous block, timestamp, nonce, and Merkle root.

- Previous Hash: Refers to the hash of the preceding block.

- Nonce: A cryptographic number used during mining to create a unique hash for each block.

- Merkle Root: The root of a hash tree representing all transactions within the block.

This structure ensures that blocks are securely linked, making it nearly impossible to alter data without altering the entire chain.

How Blockchain Works: The Transaction Process

- Transaction Request: A user initiates a transaction, which is then broadcasted to the blockchain network.

- Verification by Nodes: Nodes in the network verify the transaction’s validity using consensus algorithms.

- Block Formation: Verified transactions are grouped into a block.

- Block Addition: The new block is added to the blockchain, linked via cryptographic hashes.

- Immutability: Once added, the block becomes immutable and permanently stored.

Key Characteristics of Blockchain Technology

- Decentralization: Unlike traditional systems controlled by central entities (e.g., banks), blockchains operate through a distributed network of nodes.

- Transparency: Transactions on the blockchain are publicly visible, allowing for auditability.

- Security: Blockchain uses cryptographic methods and consensus mechanisms to secure transactions and prevent tampering.

- Immutability: Once data is recorded on the blockchain, it cannot be altered or deleted without altering subsequent blocks.

- Distributed: Blockchain’s distributed ledger ensures that no single point of failure exists, increasing resilience.

- Trustless System: Users don’t need to trust each other or intermediaries; the system itself ensures data integrity.

Consensus Mechanisms in Blockchain

Blockchain consensus algorithms ensure that nodes in the network agree on the validity of transactions. Common consensus mechanisms include:

- Proof of Work (PoW): Used by Bitcoin and Ethereum (prior to Ethereum 2.0). Miners solve computational problems to validate transactions.

- Proof of Stake (PoS): Validators are chosen based on the number of coins staked, promoting energy efficiency.

- Delegated Proof of Stake (DPoS): Token holders vote for delegates who validate transactions.

- Proof of Authority (PoA): Validators are selected based on reputation rather than computational power or stake.

Blockchain Evolution Through Four Generations

- Blockchain 1.0 (Digital Currency): Focused on cryptocurrencies like Bitcoin, providing a decentralized payment system.

- Blockchain 2.0 (Smart Contracts): Ethereum introduced programmable contracts that automatically execute when certain conditions are met.

- Blockchain 3.0 (Decentralized Applications – dApps): Enabled the development of decentralized applications running on blockchain networks.

- Blockchain 4.0 (Industrial Use): Integrates blockchain into business and industrial operations, improving supply chain management, data security, and efficiency.

Applications of Blockchain Technology

- Cryptocurrencies: Blockchain underpins digital currencies like Bitcoin, Ethereum, and others, ensuring transparent and secure transactions.

- Smart Contracts: These self-executing contracts automate agreements and reduce the need for intermediaries.

- Supply Chain Management: Blockchain improves transparency and traceability of products across the supply chain.

- Digital Identity Management: Blockchain enables secure and verifiable digital identities, reducing identity fraud.

- Real Estate: It streamlines property transactions, making them faster and cheaper.

- Intellectual Property Rights: Blockchain records ownership and protects intellectual property.

- Banking and Financial Services: Blockchain facilitates faster, cheaper, and more secure financial transactions.

Advantages of Blockchain Technology

- Increased Security: The decentralized nature of blockchain ensures data integrity and protection against cyber threats.

- Transparency: All transactions are recorded on a public ledger, ensuring accountability.

- Reduced Costs: Blockchain eliminates intermediaries, reducing transaction and processing fees.

- Immutability: Once recorded, data on the blockchain cannot be altered, ensuring permanent records.

Challenges and Limitations of Blockchain

- Scalability: Public blockchains can face delays in processing transactions during periods of high activity.

- Energy Consumption: Proof of Work blockchains, such as Bitcoin, require significant energy resources for mining.

- Complexity: Implementing and understanding blockchain systems can be challenging for businesses and developers.

- Regulatory Concerns: As blockchain disrupts traditional systems, it often faces resistance or lack of clear regulation.

Conclusion: The Future of Blockchain

As blockchain technology continues to evolve, its potential applications are expanding beyond cryptocurrencies to industries such as healthcare, finance, logistics, and government. With advancements in scalability and regulatory frameworks, blockchain is set to revolutionize how data is recorded, verified, and shared globally.